Coming into 2023, market sentiment was broadly negative following the worst year for a diversified portfolio in 40 years. In 2022, we saw equity markets fall -18% and fixed income markets drop a staggering -13% as the Federal Reserve acted aggressively to combat rising inflation. There weren’t many places to hide, and despite a market rally in the 4th quarter of 2022, market participants entered 2023 with concerns that this year would be more of the same. Many strategists were speculating that the Fed’s historically aggressive interest rate hiking policy would end in a “hard landing” and eventual recession.

Boy were they wrong…equity markets broadly rallied in 2023, with US markets up +25.96% (Russell 3000) and international equities up 16.21% (MSCI ACWI Ex USA). Fixed income markets were choppy to start the year but ended the year up 5.53% (Bloomberg Aggregate) as a result of a significant rally in the 4th quarter. The conviction in a “hard landing” fell precipitously throughout the year as inflation fell, the consumer stayed strong, and the labor market continued to show gains. Dreams of a “soft landing” (small recession) and “immaculate landing” (continued economic growth) began to take hold. The Fed added some fuel to this growing positive sentiment by indicating that they were reaching the end of their rate hiking cycle, and actually signaling a few rate cuts in 2024. This led to a significant market rally during the 4th quarter where we saw equity markets broadly up +11.15% (MSCI ACWI) and fixed income markets up 6.82%.

It is worth noting how narrow equity market performance was in 2023 however, with just seven names making up nearly all of the positive performance in the S&P 500. These names happen to be the seven largest in the market and have been referred to as the “Magnificent 7” throughout the year; Microsoft, Apple, Amazon, Alphabet, Nvidia, Meta, and Tesla. This type of narrow market leadership is not common historically, and we do not expect this to continue throughout 2024. We continue to believe that diversified portfolios with allocations to small caps and international markets (in addition to large cap equities) will be best suited for long-term growth and income.

The Federal Reserve continues to be a focal point of this market with their policy actions and commentary under a watchful eye as inflation continues to trend towards their 2% target. While the Fed continued to raise interest rates throughout 2023, long term rates were left little changed as market participants expect interest rate cuts to commence in early 2024. The Fed confirmed that cuts were on the horizon in their December meeting, with their dot plot (the survey of Fed officials on where interest rates will be at the end of the following year) showing the highest probability of three 0.25% rate cuts in 2024. While the direction was confirmed by nearly all FOMC participants, the range of how many cuts was large.

The Federal Funds Futures market, on the other hand, is currently signaling six 0.25% rate cuts in 2024. We continue to believe that the market is well ahead of the Fed and are more confident in what the Fed has projected over what the market is telling us. The dislocation between the two represents a risk that we could see throughout 2024 as the market brings longer term rates higher to meet where the Fed is at. While there are a lot of factors that go into this, the Procyon investment committee has this relationship at the top of its watchlist in 2024.

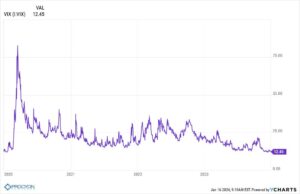

With the strong end to 2023, it is difficult to remember any volatile periods during the year. The volatility index tends to confirm this as well, falling throughout the year and ending the year at levels last seen prior to the market sell off in 2020. There was a fair amount of volatility throughout the year however, as markets tried their best to price in a number of events including: failures of Silicon Valley Bank & Signature Bank, continued war in Ukraine, conflict between Israel and Hamas, above target inflation, the inverted yield curve, and the rise of artificial intelligence.

As we enter 2024, there are a number of key topics that have our attention in what we expect to be a volatile year.

Here are a few that remain at the top of our list:

- 2024 Presidential Election – There is no surprise that this would be first on our list of what to watch in 2024. In what is currently shaping up as another Biden vs. Trump election, there will be uncertainty that leads to volatility in financial markets throughout the year. While markets tend to be forward looking and will quickly look past the election, results can have major implications on the future of companies. With debt levels soaring and the 2017 tax cuts set to expire in 2026, the next president will have large decisions to make. Leading up to the election, we expect rhetoric on hot topic issues such as health care, big tech, and the broader economy to gain market attention. As the election gets closer, we will start to get a clearer picture of what the next 2-4 years will look like. The market has historically been choppy during an election year, with positive performance later in the year once the uncertainty of the election cycle passes. Additionally, the market has historically performed best under a split government in the subsequent years.

- The Fed – While we expect the Federal Reserve to largely step out of the way in the election year, their actions and commentary will undoubtedly continue to have an impact on markets. With inflation still running above their 2% target and a strong labor market, the Fed continues to have room to act. We will continue to monitor this along with any impact on the economic picture stemming from the lagged effects of their historically fast rate hiking cycle. All in all, we believe that the Fed is closer to the end of their tightening cycle than the beginning. The market is currently pricing in several rate cuts before the end of next year. At this point, we think those expectations are a little lofty and we wouldn’t be surprised to see the Fed keep rates steady throughout much of next year.

- Geopolitical Tensions – With the Russia/Ukraine war continuing on and the rising conflict in the middle east, we believe that these tensions will likely persist throughout much of next year. There continues to be concern that these wars can spread, with other players taking action. While obviously difficult to predict, we continue to watch developments closely with a specific focus on interactions between the US and China relative to Taiwan. Reshoring of operations should help limit the impact of any conflict to global companies, but the risks still remain. We are closely watching manufacturing trends and energy prices as these conflicts continue.

As we evaluate the number of scenarios that could happen in 2024, we anticipate one of the following three to unfold:

- Optimistic – Soft landing, Inflation comes down to 2%, GDP grows, jobs remain stable.

- Pessimistic – Fed has increased rates too far already, GDP falls, unemployment increases, but inflation comes down.

- Realistic – Soft landing but, inflation stuck at 2.5% and we can live with it, unemployment goes up but not much, new rates stay higher than rates since 2007, GDP grows modestly.

We believe the positioning as it relates to these potential outcomes is first and foremost a function of the investor’s time horizon as markets can be unrelenting. However, our committee is taking the positioning that most equities, excluding the mega cap tech stocks, in the public markets are fairly valued or undervalued and we remain neutral in the face of potential headwinds. Our fixed income allocation is short, high quality, and underweight due to an overweight to cash with good yields while our alternatives allocation is overweight where appropriate given the

opportunity set.

IMPORTANT DISCLAIMERS AND DISCLOSURES:

The information contained in this presentation has been gathered from sources we believe to be reliable, but we do not guarantee the accuracy or completeness of such information, and we assume no liability for damages resulting from or arising out of the use of such information. Past performance is not indicative of future results.

The views expressed in the referenced materials are subject to change based on market and other conditions. This document may contain certain statements that may be deemed forward‐looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided herein does not constitute

investment advice and is not a solicitation to buy or sell securities.

Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, investment model, or products, including the investments, investment strategies or investment themes referenced herein, will be profitable, equal any corresponding indicated historical performance level(s), be suitable for a particular portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no

longer be reflective of current opinions or positions.

Please note that nothing in this content should be construed as an offer to sell or the solicitation of an offer to purchase an interest in any security or separate account. Nothing is intended to be, and you should not consider anything to be direct investment, accounting, tax, or legal advice to any one investor. Consult with an accountant or attorney regarding individual accounting, tax, or legal advice. No advice may be rendered unless a client service agreement is in place.

Procyon Advisors, LLC is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). This report is provided for informational purposes only and for the intended recipient[s] only. This report is derived from numerous sources, which are believed to be reliable, but not audited by Procyon for accuracy. This report may also include opinions and forward-looking statements which may not come to pass. Information is at a point in time and subject to change.

Download PDF BACK