“The intelligent investor is the realist who sells to optimists and buys from pessimists.” – Benjamin Graham, The Intelligent Investor

We are three quarters of the way through 2020 and if one fell asleep in January and woke up today the market returns year to date would look remarkably unremarkable. While investors cannot avoid the daily overload of information, many times shifting the viewer’s point-of-view from optimistic to pessimistic and back again, we have experienced notable market resilience in the face of immense difficulties. Along with that, we are now challenged to understand how behaviors and activities will be affected by this health crisis moving forward. As we edge closer to the election and re-opening fragmentation reigns, we are reminded to be realists in the face of important decision-making over the next several months.

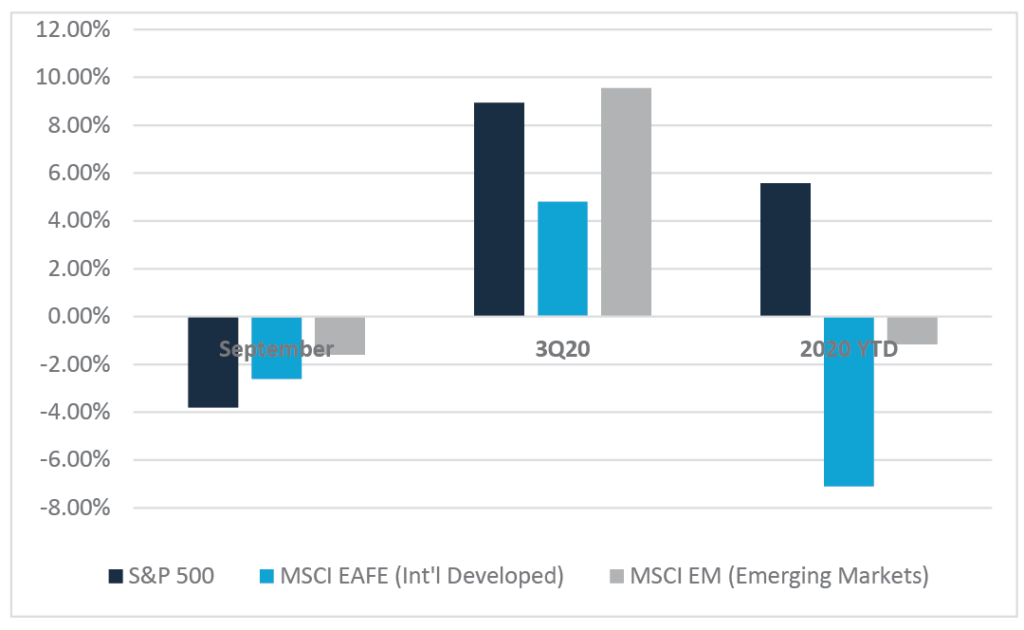

Though the month of September delivered negative returns across most asset classes, we are careful to also reflect on the full 3rd quarter and year to date returns as a broader source of perspective.

As our understanding of the impact of the pandemic evolves, our team of seasoned professionals is actively working to understand how the economy may perform in the coming quarters. Projections of third quarter GDP growth have increased from April through September, reflecting both a better understanding of changing consumer behaviors, massive reemployment, and the ability of businesses to adapt (or not) to the new environment. It is evident now that absent a major acceleration in COVID-19 cases this fall and winter, the economy will show strong growth in the third and fourth quarters. Even after this projected rebound, however, the economy will be operating well below its potential and unemployment will remain elevated. As part of the US Central Bank’s mandate and clear direction, unemployment will weigh strongly on interest rate decisions in the coming years.

We have witnessed an increase in confidence among consumers as well. As shown by the Consumer Confidence Survey performed by The Conference Board: “Consumer Confidence increased sharply in September, after back-to- back monthly declines, but remains below pre-pandemic levels,” said Lynn Franco, Senior Director of Economic

Indicators at The Conference Board. “A more favorable view of current business and labor market conditions, coupled with renewed optimism about the short-term outlook, helped spur this month’s rebound in confidence. Consumers also expressed greater optimism about their short-term financial prospects, which may help keep spending from slowing further in the months ahead.”

Much of the population’s behavior has adjusted for new norms and the change in attitude towards risk can be attributed to a few factors.

First, our understanding of the risks of contracting COVID-19 today are much better than in March. During March, our society experienced what might only be called a significant blackout period related to the lack of available information about the virus, its effects, primary targets, death rates and how it was transmitted. Secondly, the broad adaption of social distancing measures has helped us avoid the worst projections made very early on. We have seen a flight from many cities into suburbs as lockdowns and confined areas weigh on the psyche of our citizens. Through these actions we have developed an evolving attitude towards certain normal behaviors. Activities such as going to the grocery store have become much safer through these new behaviors and business adaptions.

Bond Market Activity

- Both taxable and municipal fixed income were nearly flat in September, with the BbgBarc US Agg Bond Index falling -0.05% and the BBgBarc Municipal Index moving +0.02% in The two are now up on a YTD basis by 6.79% and 3.33% respectively.

- Investors continue to reach back out into riskier fixed income sectors as treasuries fell throughout the The 10-year treasury bond yield ended the month at +0.69%, increasing 30% from the end of July.

- High yield fixed income continued to trend higher and was up +1.04% for the month. With a higher correlation to equity markets, high yield bonds were able to post positive performance during the Year to date, high yield is down 0.30%.

Global Equity

Overall US markets were weaker – well off the Sept 2nd all-time highs. For the month, the S&P was -3.9%, Nasdaq

-5.16%, and the Russell -3.8%.

In September, international markets were generally weaker with some Coronavirus flare up in Europe. HK -6.8%, Brazil -4.8%, Germany -1.4%, UK -1.7%. A couple of bright spots were Mexico +1.68% and Japan +9.7%.

Real Estate Activity

Residential real estate continues to be a bright spot. New home sales are their highest in over a decade and posted a MoM increase of 4.8%. Existing Home sales continue to rise, and Single-family home starts continue to increase.

Despite a sharp sell off at the beginning of the month, the markets have shown signs of a continued recovery as the 5-8% Biden polling lead remained consistent, stimulus talks have renewed and hopes for a vaccination continue. The resiliency in the economy and the markets continues to impress, marked by a very nice recovery into month end despite the general dismal opinion on the presidential elections and conditions surrounding President Trump’s positive coronavirus test. We look forward to more clarity on the elections, hope for progress in civil unrest and pray for progress in Operation Warp Speed.

We wish you a relaxing and safe holiday weekend, filled with autumn activities, pumpkin spice lattes, and do not forget Halloween is right around the corner!

Download PDF BACK