MARKET UPDATE: “THE BEST TIME TO PLANT A TREE WAS 20 YEARS AGO, THE SECOND-BEST TIME TO DO SO IS TODAY.” – ANCIENT CHINESE PROVERB

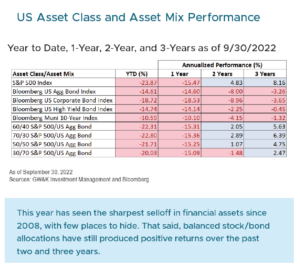

As we witnessed the most significant drawdown in wealth since the 2008 financial crisis, the first three quarters of 2022 have collectively cost investors more than $9.5 trillion from the market’s high-water mark at the end of 2021. This includes the market value declines in both the public equity and fixed income markets.

The drawdown has been felt for both aggressive and conservative investors alike, as nominal and real rates of return are negative across almost all major public markets.

In times of stress our behaviors can dictate our outcomes and remaining patient through turbulent times has been a fundamental tenant throughout our investing careers. As difficult as it may sometimes be, we find that through active management and avoiding large behavioral mistakes we can navigate through market stress quite effectively. This is predicated on the ability of investors to be patient and allow time for asset prices to recover.

What do we think about stock prices today?

Fundamentally, current valuations can help derive future expectations for market returns. For several years, valuations in equity markets appeared stretched and a protracted Fed policy of zero-interest rates helped facilitate those valuations. That was true for a very long period. If we can remember, those policies began 14 years ago with the Great Financial Crisis. Ushered in by then Fed Chair Ben Bernanke, who just recently received the Nobel Prize in Economics for that very work.

That regime appears to have ended as we enter a new, more normal, period of higher rates. As this occurs asset prices recalibrate, and stock market valuations appear to be the first casualty as the market price-to-earnings (P/E) ratio has come down along with the Cyclically Adjusted P/E (CAPE) ratio and several other key valuations measures. Now that we’re experiencing this regime change and a fundamental reset of asset prices, we can gather and interpret some data to help us discern what current levels may indicate about future returns.

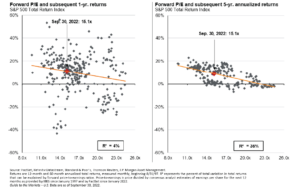

As shown on the following page, the two charts are rolling 1 and 5 year returns from August of 1997 through September of 2022. On the left axis are the returns and the bottom axis are valuations.

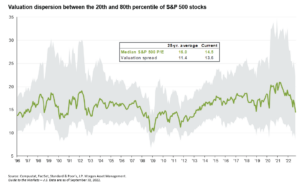

On the following chart, you can see the current forward P/E ratio for the S&P 500 is ~15.1x , and indicates positive future returns for both the 1 and 5 year time periods. This means that we are seeing a readjustment of the number of years in advance an investor is willing to pay for today’s earnings. Even the highest valuation stocks have seen a recent contraction as illustrated in the valuation dispersion chart here.

Corporate Earnings:

Our team expects a mixed bag for earnings this quarter as we see the effects of inventory buildups in reaction to supply chain lags filter through the largest firms. Input costs have come down in recent months helping to dampen some of the expense pressures in critical markets, however wage growth will continue to weigh on earnings.

While the expectations for 3Q earnings have come down this year, the reported data and forward guidance will have a big influence on returns over the course of this earnings season. Price volatility is expected to continue. We do expect that earnings in cyclical sectors will tell us a bit more about where the economy stands and how consumers are making spending decisions.

Spending decisions are of course the US Central Bank’s end target. With rapidly rising prices stressing the budgets of the general population, the central bank is focused on increasing the cost of borrowing to dampen demand, and therefore the prices of goods and services. The current rate of price increases, 8.2% from the previous year as of September, is increasingly harmful if sustained over long periods.

To combat this dynamic the US central bank is making money more difficult to obtain. The potential for continued inflationary pressures signals that this interest rate cycle could last longer than some of the rising rate cycles in recent memory. There have been six “Fed Pivots” since interest rates peaked in 1984, and while there may be some starts and stops to the recent upward trend, the trend is clearly upward. While most asset allocators have had this expectation for some time it has come to fruition very quickly in 2022.

Recession & Jobs:

The topic of a recession in the US has been debated exhaustively by economists and commentators on business news. The fundamental definition of a recession is two consecutive quarters of GDP contraction, and as currently reported that is what we experienced in the first half of this year. The debate around whether we are experiencing a recession consistent with that definition really hinges on the prevailing low unemployment numbers across the country. Be that as it may, the job market is still quite robust by all measures. For example, there are currently 1.87 job openings per job seeker (USDL, JPM) which has been a key driver of wage growth. By way of comparison, the previous peak was just before the pandemic at ~1.25 jobs available per seeker. These numbers are likely to come down as the post pandemic economy normalizes further.

Our expectation is that the unemployment rate in the US will tick higher, job openings will contract, and wage growth will moderate in the coming quarters. While this may be truer for some industries versus others, we do expect a broad moderation in the job market across the US over the next year.

Base Case:

The Procyon Investment Committee has established a base case scenario for our economic expectations over both the short and long term. Over the short-term we believe the Fed will likely continue to increase rates until one of two scenarios come about:

- CPI data trends below 6% for multiple months

- Unemployment rises above 5%

There continues to be some potential for a “soft landing” if inflation slowly reverts to it’s mean at closer to 3.5% over a 1- 3 year period, but recent data suggests that is becoming harder and harder to achieve.

Higher rates are likely to place continued pressure on equity valuations and earnings in the coming quarters and as we enter the holiday spending season. As a result, our short-term tactical allocations reflect more conservative equity and fixed income positioning.

Over the long-term, we look to relative valuations for our expected returns, and continue to believe that broad asset allocation across small, mid and large cap equities will provide higher returns in the future. Accordingly, we have increased our exposure to areas where valuations are at historical lows relative to their long-term average, as well as the quality of core portfolio investments in recognition that more effective firm management teams should fare better in an environment defined by increasing costs to do business.

We also acknowledge that markets are a forecasting mechanism and that the rally in equities will likely begin before jobs losses reach their peak. We will of course continue to monitor the changes in the economy closely as we look for compelling opportunistic investments.

In addition, we remain positioned more heavily on the shorter end of the fixed income maturity ladder with rates expected to continue moving higher. High credit quality and active management provide long-term benefits in the bond market, and we are committed to making changes where necessary. We also see the potential for credit deterioration and have reduced our investments in high-yield securities in recent quarters as a result.

In summary for 3Q22:

- We saw a continued reduction in public asset prices,

- Valuations have come back down to their historical averages after being elevated throughout the “zero interest rate environment”,

- 3Q earnings and 4Q shopping season are in focus,

- The Fed is committed to rate increases until data suggests they stop, and

- Portfolio positioning is conservative with a focus on higher

The Procyon Investment Committee is committed to providing insightful market analysis as we assess the evolving investment landscape. As fiduciaries, we are dedicated to our clients’ best interests and our principal goal is to make sure that we deliver exceptional advice to every client. We thank you for the continued trust you place in us as we help you navigate this challenging environment. If you have any questions or would like to discuss your financial goals or investment portfolio, please don’t hesitate to let us know.

Best Regards,

Procyon Partners

Download PDF BACK