Stocks saw major dispersion in the first quarter of 2023, with the Nasdaq rallying 17.1% for its best quarter since 2020. Meanwhile, Large Value lagged (+1.0%), primarily due to underperformance in Financials, which were down (-5.6%). Small Caps (+2.7%) also lagged, as Financials make up a larger percentage of the Russell 2000 Index versus the S&P 500. Overall, the S&P 500 finished the quarter up 7.5%. As shown below, five of the seven best performing stocks in the S&P 500 were in the Tech sector, while six of the seven worst performing stocks were in the Financial sector. Historically a strong first quarter bodes well for the remainder of the year. Since 1950, when the S&P 500 gained over 7% in the first quarter, the full year has never been negative.

The issues that plagued Silicon Valley Bank (SVB) are also a challenge throughout the financial industry to varying degrees. Banks like SVB saw enormous success and a surge in deposits in the years leading up to 2022, in part due to an era of zero interest rates and quantitative easing. As a result, banks invested this excess cash in Treasuries and other similar securities, but some banks reached for yield and invested in longer duration securities. A sudden pivot by the Fed away from low rates (due to surging inflation) led to large unrealized losses in these securities as yields surged and bond values decreased. Banks are normally able to use an accounting method called “Held to Maturity” (HTM) to avoid losses, as long as these bonds are held until maturity. The surge in Treasury yields since 2022 left many bank’s HTM securities massively underwater, and a run on smaller banks forced them to unload their HTM securities at a loss in order to replenish deposit ratios.

- It’s important to note the government guaranteed all deposits for SVB and Signature Bank because they were in receivership and deemed a “systematic risk exception.”

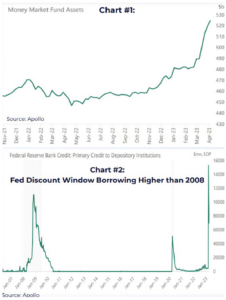

- Over the past few weeks, Banks have seen their deposits decline by a record $300 Billion. After SVB went under, some deposits that left Small Banks went into Large Banks. Other deposits moved to higher yielding Money Market Funds, with a record $5.2 Trillion in these funds (see Chart #1).

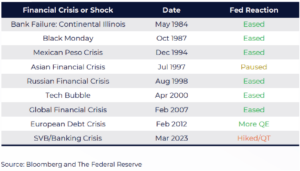

- To improve liquidity and stability, Banks utilized the Fed’s Discount Window and the Fed’s newly established Bank Term Funding Program (BTFP). Both allow Banks to borrow short-term loans from the Fed by providing collateral (i.e. Government Bonds) at Face Value, regardless of market price. This resulted in the biggest surge in borrowing using the Discount Window since 2008 (see Chart #2).

- Usage of the Fed’s Facilities resulted in a jump in the Fed’s Balance Sheet by $300 billion, despite QT.

- The Dodd-Frank Act tried to reduce concentration among Banks, but we expect further consolidation now.

- According to Apollo, tighter financial conditions and lending standards equates to an additional 150 basis points in the Fed Funds Rate. Already, Bank Lending has plummeted (see chart #3).

-

Alternative Assets are seeing continued demand from asset flows as investors look to diversify their return streams. Venture Capital and Private Equity are likely to see underperformance in the short term as multiple compression can have a lagged effect from the public to private markets, and this will likely provide liquidity in the form of supply to the secondary market. Private credit, lending, and non-residential real estate remain stable as this asset class operates parallel to bank and public market lending. We have seen a broad dispersion of hedge fund performance in 2022 with some funds logging their best numbers in many years with leveraged short positions on the bond market, while others, with large investments in Big Tech and Crypto, fell 90%+. For 2023, it is unclear whether we can have a repeat performance of hedge fund managers, or if that dispersion will narrow.

It’s not unusual for a Tightening Cycle to result in a Financial Crisis. In response, the Fed has historically either Eased or Paused. In some instances, a Recession was avoided (i.e. 1984 Failure of Continental Illinois), while other times a Recession quickly followed (i.e. Global Financial Crisis).

In the past, a financial shock/crisis has never ended until the Fed paused or cut rates. The Fed’s response to the recent Banking Crisis is highly unusual, as the Fed hiked rates 25 basis points in March and continued Quantitative Tightening. Prior to the Banking Crisis, markets were pricing in a 50 basis point hike, but financial stability took precedence over price stability. The Fed continues to be in the difficult position of trying to battle high inflation while also managing a crisis in the Regional Banking system. Procyon believes the Fed is nearing the end of its tightening cycle, especially with a deep inversion of the yield curve continuing.

In March, the Fed raised rates to a range of 4.75-5.00% and released its updated “Dot Plot,” which showed a majority of FOMC participants forecasting just one additional rate hike in 2023. The market continues to price in a much different outlook for rates, with expectations of multiple rate cuts in the second half of 2023. In looking at the past 30 years (going back to 1994), there have been five prior rate hiking cycles – including the current cycle.

In the prior four cycles, equities rallied after the last rate hike except in 2000 during the bursting of the Tech Bubble. The end of the current rate hiking cycle could be bullish for equities.

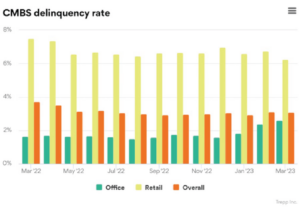

The resulting implication on the CMBS market has been a large increase in the perceived risk of those commercial loans and the widening of option-adjusted spreads. Essentially repricing the cost of borrowing for commercial borrowers, relative to other borrowers. Our committee is monitoring the broader credit markets as we see potential for pockets of risk to be identified through the current rate hiking cycle. More recently the Procyon Investment Committee dug deeper into the Commercial Mortgage-backed Securities market to gain some insight on what appears to be a potential headwind to economic growth in the US in the coming quarters. It is important to note that while the overall CMBS market has shown a steady delinquency rate over the last twelve months, we are seeing delinquencies rise in office space specifically. As borrowing rates have risen and post-pandemic work habits have taken some time to unwind, the demand for office space has not bounced back as fast as landlords would have liked.

The resulting implication on the CMBS market has been a large increase in the perceived risk of those commercial loans and the widening of option-adjusted spreads. Essentially repricing the cost of borrowing for commercial borrowers, relative to other borrowers.

Our committee is monitoring the broader credit markets as we see potential for pockets of risk to be identified through the current rate hiking cycle.

Scenarios

As we have mentioned in previous commentary, there are some key tenets we are basing our current Macro Economic scenarios on and a quick review is as follows:

- We believe the Fed. If the FED says they will fight inflation, then they are committed to conducting policy with that outcome in focus. The Fed market “put” is gone.

- In order for interest rates to remain as they are i.e. the end of the hiking cycle one of two things needs to occur:

- Inflation (CPI) falls below 4% on an annualized basis and is sustained for several readings

- Unemployment will need to go above 5% and be sustained for multiple readings

- Current CPI is 5% Annualized as of March 23 and the unemployment rate is currently sitting at 3.5%

- In order for Interest rates to decline:

- A deep recession needs to occur for the FED to consider inflation a lesser threat to prosperity.

- Major bank failure: a major bank failure would create a sufficient decline in economic activity as to counteract inflation and would result in a tightening effect.

- Recent regional bank failures may provide some economic slowing. The overall environment in the markets continues to present a unique landscape. While we continue to see macroeconomic expectations overwhelming the headlines, we continue to focus on diversification, quality and cash flows as we act prudently in this challenging period for our clients. As you enter new periods in your life with new goals and evolving risk tolerances, we encourage to contact your advisor as proactive planning and risk management are key values at Procyon. Thank you for the trust you place in us.

Download PDF BACK