As the Russia-Ukraine war continues and uncertainty builds across global markets, we have compiled some thoughts for you regarding the direct and indirect risks we see unfolding, including sanctions, oil prices, commodities, and investor sentiment. Of course, it goes without saying that this situation is very fluid, and things can change by the hour.

What does Vladimir Putin want?

It’s a question a lot of people are asking. At this point, there really appears to be no path for a “victory” – however one defines that. For starters, Putin wants Ukraine President Volodymyr Zelensky out, and the annihilation of the Ukrainian military. Neither has been achieved as of today (March 8). Therefore, he appears to need an off ramp and recognizing that he really has none, is now really being compelled to double down.

What is Putin’s list of demands? He wants Ukraine to concede Crimea to Russia along with a land bridge to Odessa. The Donbas region will also need to be recognized as Russian. Furthermore, Ukraine will also need to make a commitment not to join NATO. Putin also ultimately wants regime change as well but ousting Zelensky and installing a puppet government will never yield authority or credibility in Ukraine. With the tenacity and will of the Ukrainian people, he will never be able to govern Ukraine with an occupying force. It will be nearly impossible.

Longer term should Russia continue its military push, we could very well see the Zelensky government move to Lviv and then to Poland where they could operate in exile. If Russia’s occupation fails, the Zelensky government could then return.

Unintended consequences of Russia’s invasion

- The US, UK and EU are now unified like never before

- NATO has been revitalized and has a new outlook on life

- Ukraine is being pushed more and more to the West

- Military spending in Europe is now expected to ramp back up

- The national “debt brake” that limits borrowing in countries like Germany and others across the EU might be amended to allow more government-financed spending on Defense

Sanction effects

The goal of the West is to restrict Russia’s economic and military development to limit Putin’s ability to continue his current pursuits, and further repeat this move in the future. The immediate effect is likely to push Russia more and more eastward to become more dependent on China.

With the US move to ban high-tech exports such as semiconductor exports to Russia, Russia’s attempted shift from a fossil fuel-driven economy to a tech-based one faces headwinds. We suspect Russia will likely turn to Chinese chip technology, but the Chinese chips are generations behind the US alternatives.

For the sanctions to be effective, the Russian population will need to blame Putin for their hardships, not the West. We’ve already seen the Duma approve a 15-year prison sentence on anyone reporting any alternative narrative to the war other than the farcical ones approved by the Putin regime.

While the multilateral financial sanctions ramped up quite quickly, the more eye-opening development has been the self-sanctioning taking place by the private sector. Multinational firms are choosing to divest their Russia ventures, as well as refusing to do business with Russia-linked firms.

Sanctions are an important tool for negotiations – think of them as a carrot and stick approach:

- If you do this, we will do this. If you withdraw from Ukraine, we will rescind banning your banks from

- But with Putin seemingly doubling down, the odds of the sanctions becoming permanent continue to

- From a technical perspective, Europe must reapply these sanctions every 6 months and for the US, it’s every

- And with self-sanctioning, reversals may never even We’ve already seen many large oil names permanently exiting the market and many other companies suspending sales with no guarantee these decisions will be reversed anytime soon.

- The question then shifts: With rising energy costs, how long will the population be willing to assume the financial hit before they start to withdraw their support for their local politicians?

Energy exports: the Holy Grail

- Given that the US does very little business with Russia, unilateral sanctions would not be nearly as Europe needs to be the driving force behind this.

- A US ban of Russian gas imports could begin to drive a wedge between the US and its Western

- Europe limiting or embargoing Russian imports is

- The impact across the EU varies from product to

- Because of this, it will be challenging to find a consensus across all member EU states

- The EU itself does not have the ability to impose energy policy on national

- As such, any agreement on the direction of limits or embargoes would need unanimity across all member states unless some were prepared to go the course

- The move to remove some Russian banks from the SWIFT payment messaging system was calculated, as Western allies have been loath to choke off the Russian energy

- The incremental risk – Putin decides to stop supplying gas to

- Think about it – he is receiving revenues from these sales that he simply cannot use. So what’s the point?

- Offsetting this backdrop – winter is almost over, and it has been less

- Should a ban persist, however, this would prevent gas reserves from being stockpiled for the next winter

- While the US and its allies have not yet unilaterally imposed penalties on Russian oil and gas, the self- sanctioning aspect has made an impact:

- Russian oil loadings for March show a sharp drop with a number of ship owners reluctant to

- The extent to which this self-sanctioning accelerates and widens, we believe, will be a key linchpin in the severity and duration of the energy

Commodities crunch

Oil price increases could certainly bite into global growth and cause further inflationary pressures. But here are some other commodities that may be at risk:

- Platinum and palladium – impacting catalytic converters and putting auto production at

- Neon – a major export from the region and a key input for semiconductor

- Wheat, corn, and sunflowers are all at

- Many emerging economies are wheat importers and likely to be hurt more from rising food costs. In fact, Egypt, Indonesia, and Turkey are the largest wheat importers in the

- Ammonia – with natural gas prices on the rise, it is now becoming cost-prohibitive to

- Potash – Russia and Belarus account for about one- third of global trade in this commodity – a key ingredient in

How can the world replace oil supply?

- Should Russian oil get cut off, there are some means to replace the

- Iran nuclear deal – Iran has some 180 million barrels ready to go, sitting on floating ships already. They could also ramp up a large amount of supply over the course of a year. So, it seems that it would be in Russia’s best interest to make fresh demands here to slow the progress of negotiations – which is exactly what they are doing.

- Global Strategic Petroleum Reserves (SPRs) stand at about 16 billion barrels, with 1.5 billion of that held by governments. If needed, roughly 60 million barrels could be delivered per month.

- OPEC has spare capacity to ramp up some 6 million barrels per day.

- US shale could increase – but producers have commented that they cannot produce output fast enough to compensate for lost Russian oil, citing lack of labor and raw material issues like steel and cement.

- Libya’s political crisis is causing output to

- The US has sent a delegation to Venezuela – the highest-level trip in years. The reasoning, it seems, is to isolate one of Moscow’s remaining allies in the world, as well as possibly replace Russian oil

Oligarch offensive

Western countries have begun creating task forces to determine which Russian oligarch owns what. Jets and yachts being seized makes for good theater. And the court of public opinion is certainly having an impact here, with many high-profile seizures hitting the news in the past week. But will the Russian elite apply enough pressure to the Putin regime to effect change?

Thus far, the answer is NO. Most oligarchs have called for an end to the escalation but have fallen well short of criticizing Putin. What’s their upside in doing so? They know who made them rich and they know who can make their lives difficult.

Demise of the US dollar? Not so fast

With the US dollar becoming weaponized, there has been quite a bit written about the overall impact. The common thread is that more and more countries will begin to move away from the USD and weaken its status as the world’s reserve currency. We’ve heard this for decades now and it has been nothing more than clickbait.

China’s CNY has been the rumored replacement for those seeking diversification. We believe the flaw in this logic is that the CNY is simply not a fully convertible currency. With capital restrictions on the currency, it hinders its liquidity, making it a nonstarter. CNY accounts for just 3% of all foreign currency transactions – while the USD accounts for over 40%. Also, to replace the buck on the global stage you would have to replace contracts and payment systems that have been in place for years. This would be a decade-long venture and not something that can be done overnight.

More importantly, in times of global crisis, having one currency dominate the international financial system makes it easier to backstop the system.

With the Fed always standing at the ready to provide global liquidity for the USD, this has been the saving grace time and time again, preventing a major collapse of the global financial system. We believe this backstop is an important misunderstanding for those calling for the end of the US dollar as the reserve currency of the world.

Market perspectives

- From February 24th, 2022, the day Russia invaded Ukraine, through March 9, 2022 US equities as measured by the S&P 500 are -0.21%. Up until now, Russia has been more of a news event for US firms rather than an economic

- Much more relevant has been the pending shift in monetary policy as managed by the US Federal Reserve

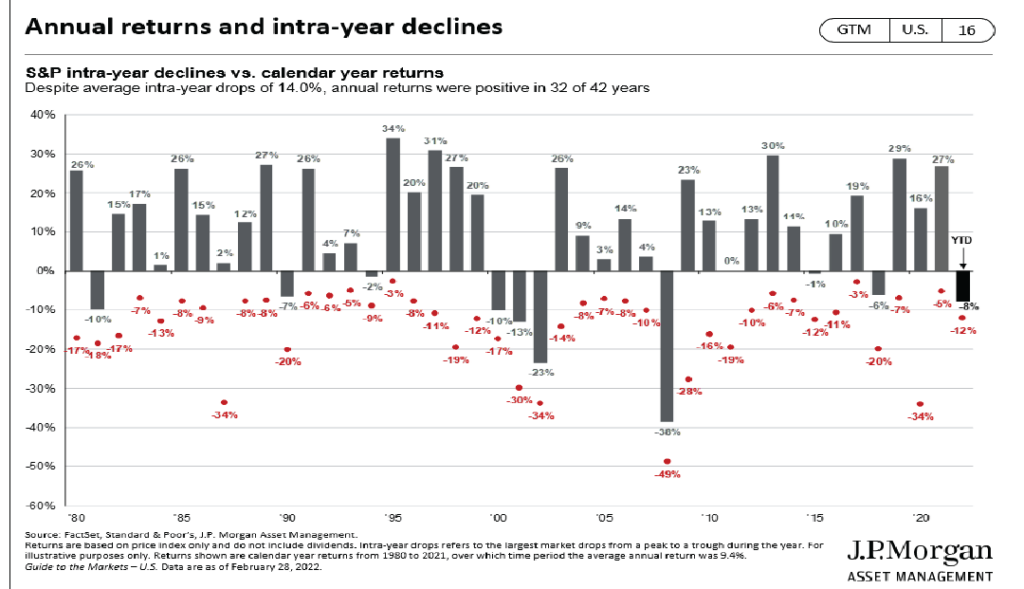

- Historical intra-year declines also help remind investors of the actual volatility that occurs in the public markets:

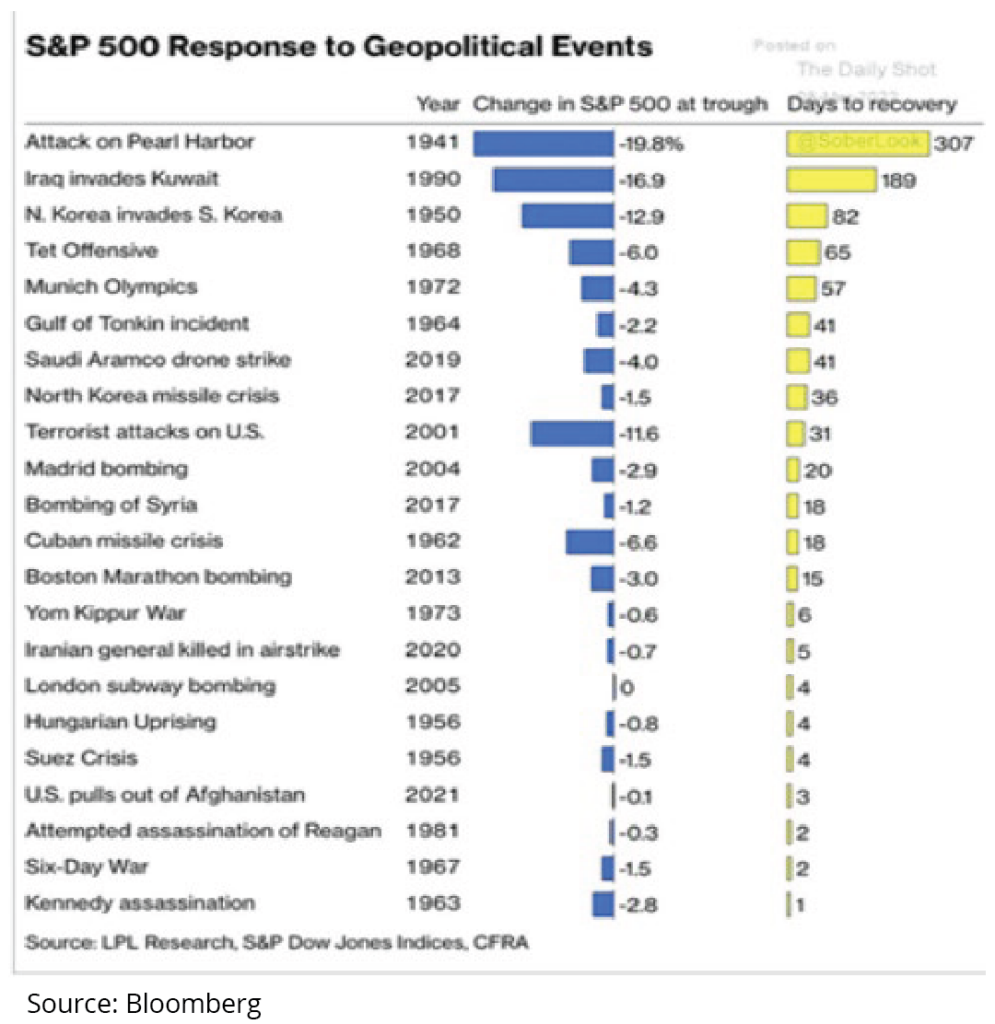

- Unfortunately, we can also review statistics regarding large scale global warfare and terrorism as well as its effects on financial market

- The euro continues to slip relative to the dollar with higher oil This creates the doom loop – oil prices rise, EUR weakens which puts increased upside pressure on inflation as a weaker EUR makes imports more expensive. Also, commodities are priced in USD and rising prices against a falling EUR only exacerbate the issue.

- Surging prices across all commodities will eat away at consumer purchasing power and intensify the inflation

- Keep in mind, however, that US household and corporate balance sheets have never been better – helping to cushion rising

- Stagflation calls might be getting a bit ahead of themselves in the Nominal growth is at a much higher starting point these days, and this should not be forgotten. Real rates are still negative. And the US is now a major oil producer, not importer.

- Energy has turned from unloved to crowded. We think any resolution could see a sharp correction in energy prices given

- Financial contagion still seems muted, and the odds of a Lehman-style meltdown remain

- Europe is the most exposed – there are upside risks to inflation and downside risks to growth. Plain and Financials may also be at risk, not from Russia exposure, but from slower economic growth.

Big picture themes

Overall, it is tough to see a resolution of the Russia- Ukraine crisis anytime soon. We expect it could be several more months. With that in mind, the macro themes we expect to play out include:

- Increased defense and cybersecurity spending

- Elevated commodity prices for an extended period

- Supply chain headaches persisting

Final thoughts

Will Putin declare war on a NATO country? This would certainly provide him additional cover, framing some “incident” to justify actions to the Russian people. The upside to this: NATO is aware and will likely not play along. Again, this unfortunate situation is very fluid, and things can change by the hour. With that in mind, our views and market perspectives may change as well.

Procyon’s Investment Committee is carefully digesting the information as it is produced. We will be watching the economic readings and high frequency data as it continues to provide us insight into areas of the market where opportunities lie and where risk may be increasing. We are interpreting this shock to the geopolitical landscape as it happens in real time and are careful not to pretend to know every possible outcome as we balance the need for capital preservation, income and growth. However, we understand our clients better than anyone and are locked into making sound and prudent decisions for them as we navigate the rough seas of 2022 and beyond.

We appreciate your continued trust and for taking time to read our intra-quarter update.

Best Regards,

Procyon Partners

Download PDF BACK