2021 was a recovery year for this economy. The “reopen” trade was on and it was time to see if those big tech companies who benefitted so much due to the skyrocketing demand for everything technology, could in fact continue their limitless trajectory. The businesses who were previously forced to close spent the year reopening and readjusting their business plans. We hope those clients who were affected in this manner in 2020, were able to spend 2021 taking advantage of opportunities as entrepreneurs do.

What’s Driving Markets?

The influence of big tech on market performance has been increasingly heightened over the last 12 months. Only 7 companies currently comprise 27% of the S&P 500 Index. The combined market values of Apple Inc, Microsoft, Alphabet, Amazon and Meta Platforms, stand at $10.1 trillion as of end of the year. That is up from $7.5 trillion from the start of the year. That 35% gain in market value exceeds the gain of the Dow, S&P 500 and Nasdaq Composite for 2021, which was another strong year for markets across the board.

This run puts a larger portion of the market under the sway of a few big names. The aforementioned five — along with Tesla and chip maker Nvidia — now comprise more than 27% of the S&P 500’s total value. And that seems likely to grow even further. Apple alone is on the cusp of reaching the $3 trillion mark, and at least 13 analysts have price targets on the stock that would put the company’s market value well past that milestone. Further, Wall Street’s median price target of $4,000 for Amazon’s shares would put the e-commerce giant past the $2 trillion mark—up 17% from its current value.

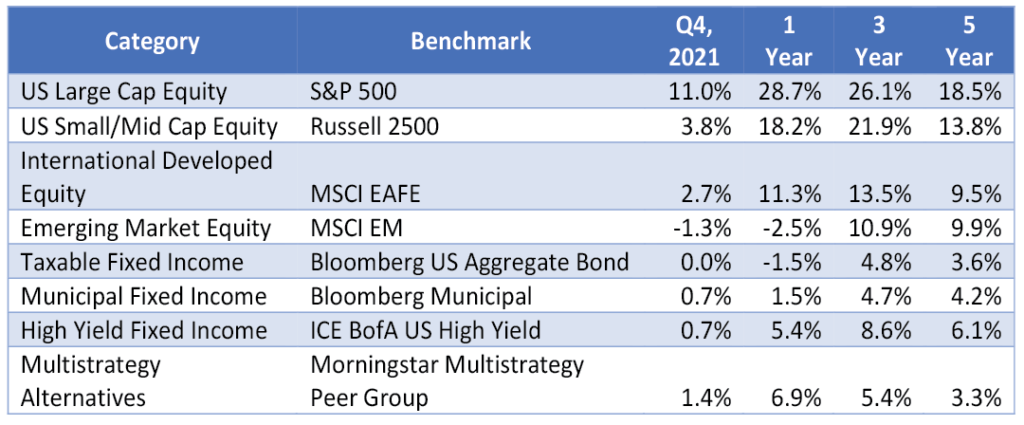

The year also closed with yet another quarter of strong performance, which has become a familiar sight since the market pullback at the onset of the pandemic in 2020. In Exhibit 1, you can see performance for many of the major asset classes across different time frames. The US has led the way and the 4th quarter was no exception.

International market performance was mixed in the most recent quarter and continues to trail the US over the longer term. Within the fixed income markets, rising yields created a broad headwind for the taxable fixed income space (treasuries, corporate bonds, securitized products, etc.) however upgrades to municipal credit qualities and limited supply created a tailwind for municipal bonds. This resulted in positive performance for municipal bonds while their taxable counterparts were negative for the year.

Since the onset of the pandemic and the initial decline in the equity markets, fiscal and monetary stimulus have supported seven consecutive quarters of equity market advances. This has left many investors in a strong place heading into 2022 and has created, for better or for worse, a sense of comfort in a level of risk that may or may not be appropriate.

To provide some context, we believe the most influential factor driving performance over the last couple of years has been monetary and fiscal stimulus. On the fiscal side (Government action), nearly $6 trillion in COVID related stimulus has filtered through the system and further action on this front continues to be discussed. Additionally, the $1.2 Trillion infrastructure package has been passed and its details have largely been priced into the impacted industries.

As far as monetary policy (Federal Reserve action), the Fed has set forth a path to ending their bond buying program and starting to tighten the money supply through the eventual raising of interest rates.

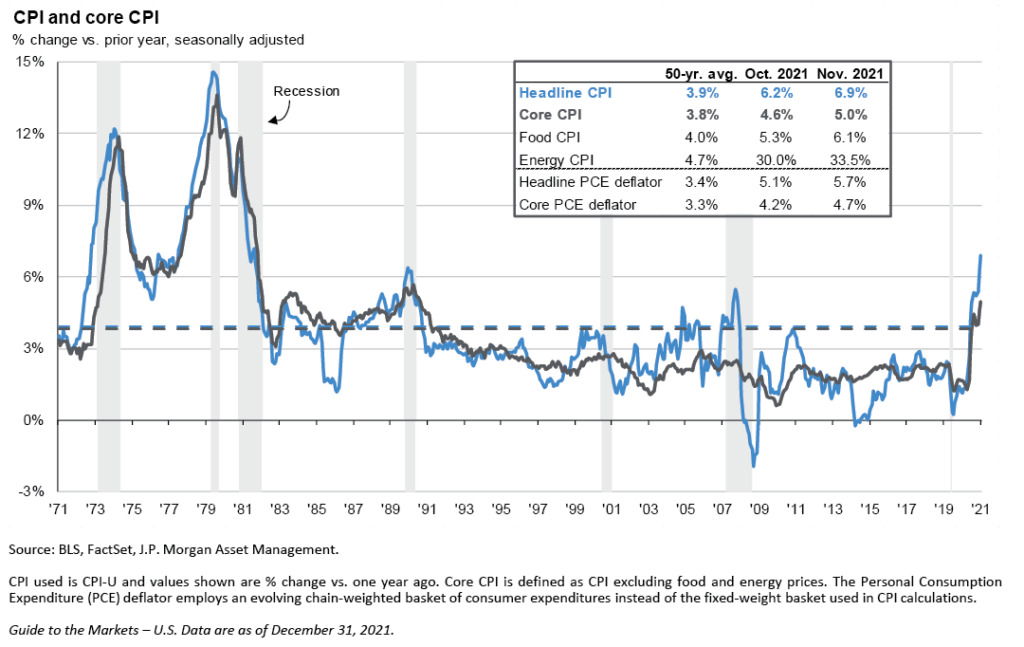

A hotter and more persistent inflation rate, as measured by CPI (above) has accelerated their plans and 2022 appears as though it will be a pivot point to begin tightening monetary policy.

As the Federal Reserve removes the “punch bowl” we are left with a market that appears to have limited drivers of future returns. When that is the case, you must turn to the market fundamentals to ensure that you continue to hold strong companies, with reasonable valuations, considering the change in policy stance. On the following pages we plan on updating you on some of these fundamental drivers, our economic scenario assumptions, and some commentary on what to expect in 2022.

Economic Backdrop:

Let’s first discuss the background that the Federal Reserve is working with entering 2022, and what’s really paving the way for this more hawkish policy stance. The Fed operates under a dual mandate of full employment and price stability.

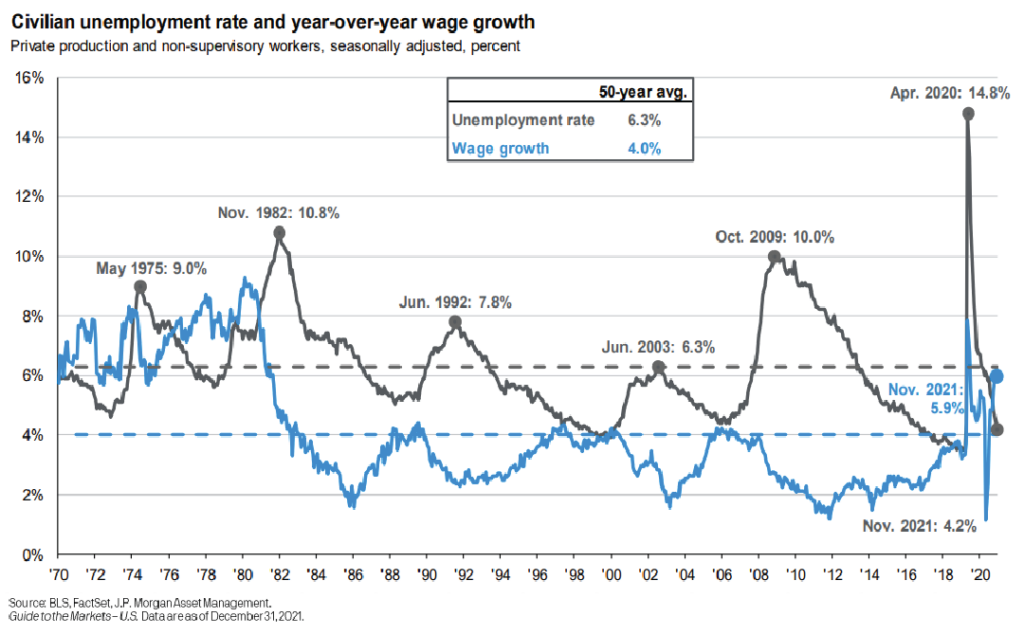

On the employment side, there has been significant improvement in the unemployment rate since the highs last April, and while there continues to be some slack in the labor market, it is currently a source of economic strength. From a price stability standpoint (more often referred to as inflation), prices across many sectors of the economy continue to be on the rise.

As we discussed during our previous commentary, these higher prices have been driven by a variety of forces including, but not limited to, supply chain bottlenecks.

Inflation continues to be on the rise year over year, with the most current reading showing an increase of 7.0% from the year prior.

These higher inflation readings coupled with the strong labor market have given the Federal Reserve the ability to act in line with their dual mandate by tightening monetary policy efforts in order to combat higher prices across the economy.

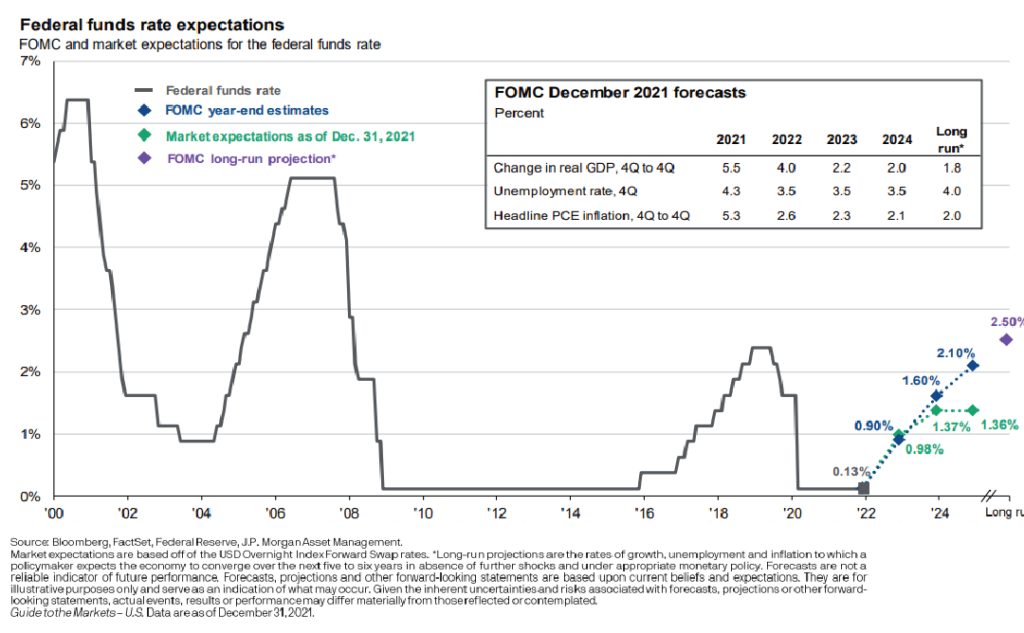

The market has reacted in line with Federal Open Market Committee (FOMC) projections at this point, pricing in roughly three 25-basis point interest rate hikes by the

end of 2022. The market has yet to price in longer-term rate hikes to this point, possibly signaling that they believe the Fed’s near-term efforts will be enough to combat the higher inflation that we have seen.

As the Procyon Investment Committee continues to dissect the signals provided by the US Central Bank, equity markets, rates and the ever-evolving public health crisis that began almost two years ago, we have developed a set of scenarios that represent the potential outcomes we face in the coming quarters and beyond:

Base Case – Continued Incremental Improvement

Our base case scenario is our investment focus and helps inform our decision-making in the coming quarters. We view this as the most likely scenario to play out given the short, but vast amount of data generated over the recent pandemic:

- No major interest rate surprises impacting the bond or stock markets

- Inflationary pressure begins to subside and does not negatively affect GDP growth in any material

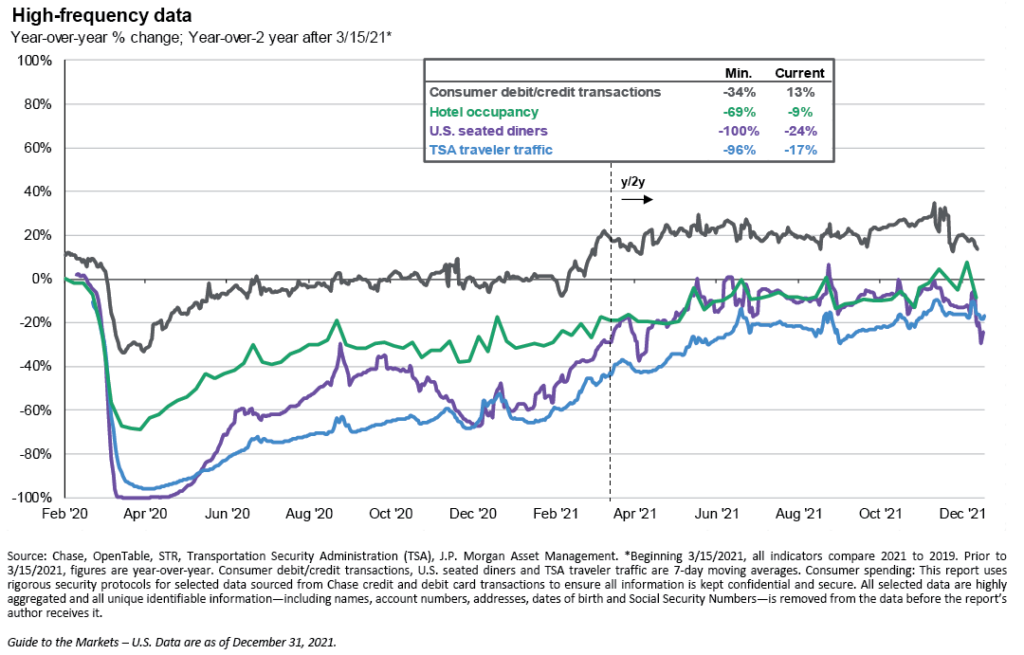

High-frequency data

Year-over-year % change; Year-over-2 year after 3/15/21*

Source: Chase, OpenTable, STR, Transportation Security Administration (TSA), J.P. Morgan Asset Management. *Beginning 3/15/2021, all indicators compare 2021 to 2019. Prior to 3/15/2021, figures are year-over-year. Consumer debit/credit transactions, U.S. seated diners and TSA traveler traffic are 7-day moving averages. Consumer spending: This report uses rigorous security protocols for selected data sourced from Chase credit and debit card transactions to ensure all information is kept confidential and secure. All selected data are highly aggregated and all unique identifiable information—including names, account numbers, addresses, dates of birth and Social Security Numbers—is removed from the data before the report’s author receives it.

Guide to the Markets – U.S. Data are as of December 31, 2021.

- COVID variants continue to be present, much like the Flu, and the economy continues to adapt to that reality more effectively

- Vaccines, and treatments, continue to improve (see below)

Overreaching Fed – Worst Case

Under the circumstances outlined here we would expect a decline in equity prices, a quick reversal in interest rates and a reset in the economic growth achieved over the last several quarters. While we feel this has less likelihood of occurring, there is some evidence that the Fed has done this in the past. Most recently in 1999/2000 as a reaction to what was coined by then Fed Chair Alan Greenspan “irrational exuberance” at the time. Markets can force the Fed’s hand in this case and the consequences are often a contraction of GDP:

- Fed hikes rates too high, too soon

- Another, more threatening COVID variant arises

- Demand for goods and services dries up quickly

- Unemployment rises

- Gov’t has limited tools available

- GDP contracts late in 2022, early 2023

- Housing begins to reverse

- Geopolitical issues remain

Surprising Resilience – Better Than Expected

We have been surprised several times in recent history at the market resilience in the face of a dramatic economic backdrop. While that is true, it is mainly centered around the idea that the government can step in whenever needed. If we find ourselves in an economy that continues to rapidly improve there would potentially need to be a set of global catalysts propelling it. Some of these could include:

- Virus subsides, COVID variants less threatening

- Political environment cools

- Supply chains reestablish efficiency

- Interest rate increases are effective

- Healthcare recovers

- Global economy resumes rapid growth trajectory

Staying Vigilant

As 2022 begins we are remaining increasingly vigilant due to some of the major divergences in normal market returns across the globe.

For example, the US markets have outpaced the rest of globe over the last 10 years but not during the 15 years prior to that. While we recognize that the fundamentals of the US economy have played a large part in the outperformance, we also recognize that economies operate in cycles.

While 2022 may prove challenging due to some of the issues we’ve mentioned above, our long-term expectations remain intact.

We have taken steps to position your portfolios in line with our expectations for the markets, as well as your personal goals. Remaining ever-vigilant to market changes as the world adjusts to some new version of normal is our role over the coming year.

Thank you for the trust you place in us.