As we reflect on the markets from 2022, we are forced to think back a bit further to the initial onset of zero rates and Fed balance sheet expansion that began more than a decade earlier. Through several cycles both economic and geopolitical, including a period of rapid globalization beginning in 2009, low inflation persisted in the aftermath of the Great Financial Crisis through most of the 2010s. Interest rates were headed higher for a short time to correct the glut of liquidity when the Covid-19 Pandemic led us back down the road to even easier liquidity and lower rates.

2020 and 2021 saw the benefits of these efforts with massive gains across most asset classes as liquidity, in the form of both monetary and fiscal support flooded the economy and markets. Economies around the world closed and reopened as they battled waves of Covid-19; all while seeing demand for countless consumer products increase around the globe.

As the demand pressures mounted during 2021 Treasury Secretary Janet Yellen made the distinction that the visible price increases were “transient”, and the core measures of inflation were more stable. As we now understand, “transient” is no longer an appropriate term to characterize the current inflationary environment. In 2022, we saw the Federal Reserve increase rates at a pace never seen before as they attempted to stomp out the inflationary pressures becoming embedded in the US economy. We have seen asset prices react negatively across the board as a result of the tightening of monetary policy.

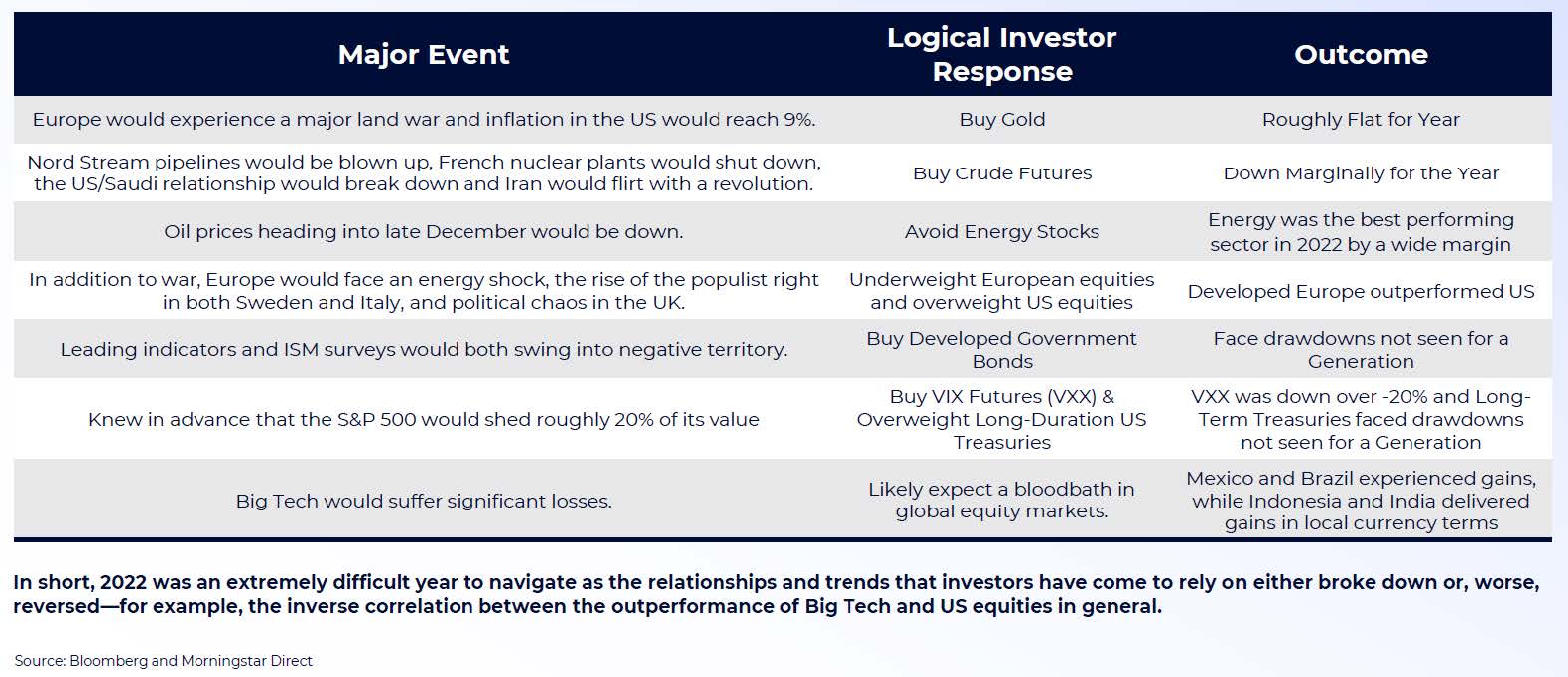

As we review 2022, it’s clear that the implications of investor responses around major events can become complex. On the following page we’ve included an interesting exhibit that summarizes how an investor may have responded to major events from last year, and how the market subsequently reacted as well.

The Fed’s Fight Against Inflation

After a 7.1% YoY CPI reading in November, the Fed slowed down its level of rate hike to 50 basis points (from 75 bps). Beginning in 2023, the Fed also slowed its rate hike to 25 basis points, starting at the first Fed meeting on February 1st. Despite the slowdown in the size of rate hikes, Fed Chair Powell has been firm in his stance of expecting higher rates for longer. While the market expects rate cuts in 2023, the FOMC’s latest quarterly projections highlight the Fed Funds Rate ending 2023 at a level of 5-5.25%.

China’s COVID Policies

China maintained strict Covid-policies in 2022, resulting in a slowing of the world’s second-largest economy and even civil unrest. Late in Q4 2022, reports surfaced that China was planning to significantly roll back these strict policies in early 2023. Since then, China has scrapped its 8-day inbound quarantine requirement for travelers, facilitated visa applications for foreigners, and stated there would be no limit to gathering in public. These early attempts to reopen have been met with a surge in COVID cases throughout the country, testing the government’s commitment to this shift in policy.

Russia-Ukraine War

The Russia-Ukraine War continues with no end in sight. Along with geopolitical concerns, the War has destabilized the energy & commodities market, particularly in Europe. Further escalation with nuclear weapons remains the biggest threat. A ceasefire remains unlikely in the short-term. Russia remains adamant that Ukraine recognizes annexed territories such as Donetsk & Luhansk, while Ukraine refuses to cede territory to Russia in any negotiations. Longerterm, the health of the Russian Economy, Army, and Vladmir Putin could be a catalyst for an end to the War.

A resolution to any of these could be a bullish for the markets in 2023.

The December CPI report showed inflation decreased to – 0.1% month-over-month, its lowest level of 2022. Inflation is down from a peak level of 9.1% in June 2022, as the Fed has undergone one of the fastest hiking cycles in 40 years (from roughly 0% to 4.50-4.75%). Goods inflation has continued to decelerate (i.e., used autos), but rent prices and wages are proving to be stickier. Wage inflation is of particular focus to the Fed, as it attempts to cool down a tight labor market. Along with raising rates, the Fed is draining liquidity in the system through Quantitative Tightening. As described at the beginning of this commentary, the Fed responded to previous shocks to the financial system (2008 & 2020) with “Quantitative Easing”; and the Fed Balance Sheet ballooned from less than $1 Trillion in 2008 to roughly $9 Trillion. In June 2022, the Fed officially reversed course and turned to Quantitative Tightening by letting Treasuries & Mortgage- Backed Securities mature without reinvestment. Finally, another tool at the Fed’s disposal is the use of forward guidance. At its December 14th meeting, the Fed released projections that showed FOMC participants expected rates to finish 2023 at a range of 5-5.25%. This was higher than anticipated, but perhaps even worse, this forecast implied no rate cuts in 2023 (differing from market expectations). This forecast was a major catalyst for the year-end selloff.

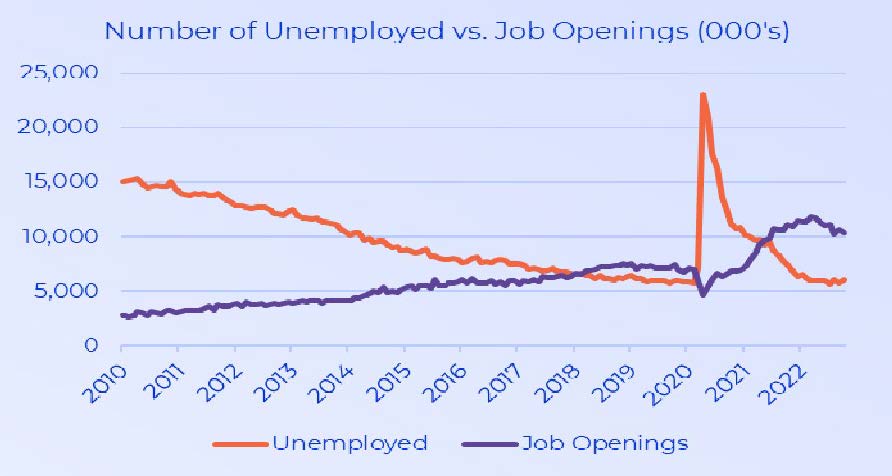

The Good: Labor Market

One constant strength in the overall economy in 2022 was the Labor market. Nonfarm Payrolls have been resilient all year despite negative headlines regarding layoffs (specifically in the Tech sector) and job openings still outnumber the unemployed by roughly 4 million. This is illustrated in Chart 1 below.

The Bad: Equity Market

Equity markets were quite resilient in the face of geopolitical worries, lockdowns in China, and the fastest tightening cycle in decades. Still, 2023 earnings expectations have been revised downward, and dispersion remains high. Large Value (-7.5%) outperformed Large Growth (-29.1%) in 2022 by the widest margin since 2000, and Energy was the top performing sector (up 65.7%), while Communications was the biggest laggard (-39.9%).

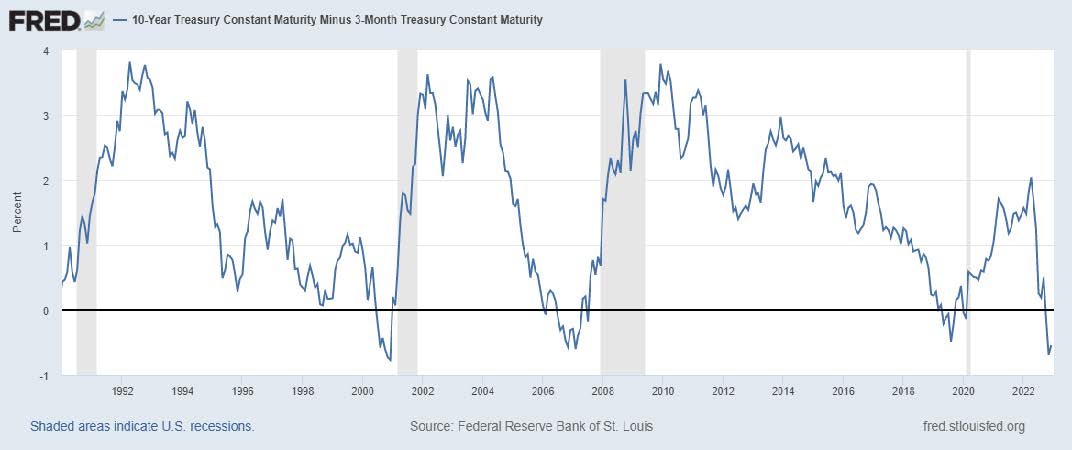

The Ugly: Bond Market

Bond markets experienced one of their worst years in history, as treasury yields surged. The 2-year Treasury yield spiked in 2022 from a low of 0.73% to a peak of 4.41%, while the 10-year yield rose from 1.52% to 3.88%. Even more concerning, a large majority of the Treasury curve is inverted. While not every yield curve inversion signals a Recession, the 10 year-3 month yield curve is deeply inverted by 54 basis points – which is its most inverted level since the Financial Crisis and Tech Bubble (see Chart 2).

Looking Ahead to 2023

In 2023 we expect the US Federal Reserve will face a choice between accepting a higher average level of inflation (3.5- 4%) or drive the US economy towards recession by sticking to their 2% inflation mandate. By contrast, most other major economies have already passed this junction, and have made their choices. In Europe, the choice was a recession, and it was not made by governments or central bankers but imposed by Vladimir Putin. In China, the choice of recession was driven not by economics but by the draconian politics of Covid. Japan’s 30 years of deflation made inflation the obvious choice. Britain, meanwhile, has bounced from Liz Truss’s tolerance of inflation to recessionary austerity under Rishi Sunak. The US is unique in having a central bank, a government, and most major sell-side Economists all arguing a painful choice will not be required between high inflation and severe recession. If this is right, and the US reduces its inflation without experiencing a severe recession—and without even imposing positive real interest rates—it will be an unprecedented achievement. But if the belief in painless disinflation is wrong, the US economy and financial markets will need to adjust when this choice between recession and inflation becomes unavoidable. The biggest challenge for financial markets is that the prospect of 2-3.5% inflation is not in the foreseeable future. Markets keep expecting a dovish Fed, but the Fed has told us they will tighten to a terminal rate of 5-5.25%. Ultimately the big question is whether the Fed will accept a higher plateau of inflation of 4+% vs the original 2% target? The Fed is trying to project an image of hawkishness but also looking to avoid a severe recession at all costs.

Investment Implications

-

If investors accept that there will now be a higher US inflation plateau, that means higher US 10-year yields. This adds risk to the long maturities of the bond market.

-

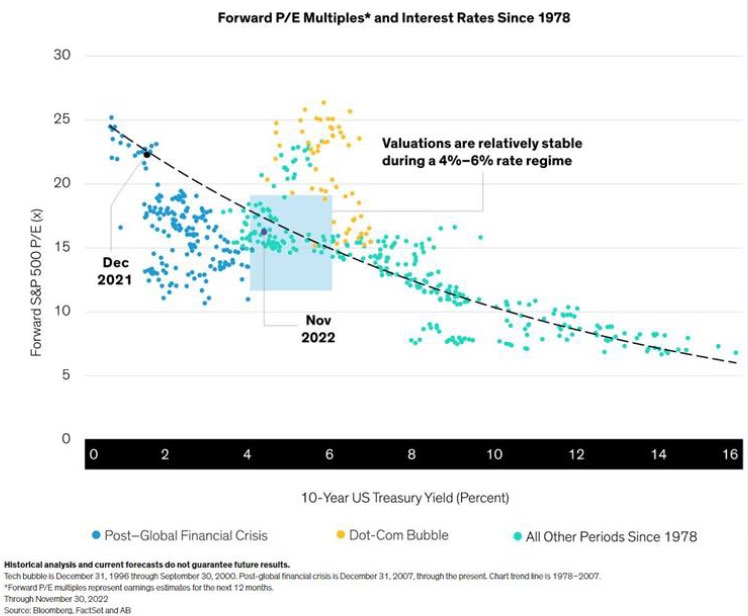

U.S equities have seen severe valuation compression – especially in the Tech sector. Given the move in short risk-free rates, it appears that this valuation compression is rational and justified. For 2023, we believe earnings becomes the focus for investors as the ability to manage through a higher rate environment becomes evident.

-

Two widely respected names in the industry, David Tepper and Jeremy Siegel, have vastly different forecasts for 2023. On the bullish side, Jeremy Siegel believes the market deserves a 20x multiple and there will be upside to 2023 Earnings (i.e., $240), which would result in a possible S&P 500 price of 4,800 (20 * 240 = 4,800). David Tepper, on the other hand, is bearish and believes the market deserves a 12x multiple on lower 2023 Earnings. If we use $225 for 2023 EPS, this would result in an S&P 500 price of 2,700 (12 & 225 = 2,700). These two examples show the discrepancy in forecasts for next year.

-

A market multiple of roughly 16-17x next year’s earnings is fair based on interest rate levels (see chart 3), but 2023 Earnings Expectations may continue to be revised downward as higher interest rates take their toll on the economy.

-

Equity rotation from Growth to Value is a continued focus as the US economy stays stronger for longer and China reopens. Major long-term rotation continues from Growth stocks/COVID gainers to Value stocks with growing earnings expectations. We remain cautious on Large Cap Technology. This sector is valuation-challenged at a time when fundamentals, especially around online advertising, and social media, are still deteriorating and competition is increasing. Additionally, we continue to think that globally, greater government regulation of Tech is increasingly on the table at a time when global geopolitical competition is heating up.

-

US Small Caps are getting interesting for long-term investors. The Russell 2000’s forward 12 months P/E ratio has fallen to 10.8x, its lowest level since 1990 and 30% below its long-term average. On a relative basis, the Russell 2000’s forward 12-month P/E is trading at the lowest level versus large-cap stocks since the Tech Bubble.

-

China and commodity producing EM’s should outperform the US and Europe. Cyclical hedges that might work as the dollar weakens, include select EM and Commodities (such as Oil and Copper). Most investors, regardless of region, are overweight dollar-based assets. This decision has been the right one in recent years, but the technical picture is indicative to us that we should add additional exposure in the form of select EM markets.

-

Alternative Assets are seeing continued demand from asset flows as investors look to diversify their return streams. Venture Capital and Private Equity are likely to see underperformance in the short term as multiple compression can have a lagged effect from the public to private markets, and this will likely provide liquidity in the form of supply to the secondary market. Private credit, lending, and non-residential real estate remain stable as this asset class operates parallel to bank and public market lending. We have seen a broad dispersion of hedge fund performance in 2022 with some funds logging their best numbers in many years with leveraged short positions on the bond market, while others, with large investments in Big Tech and Crypto, fell 90%+. For 2023, it is unclear whether we can have a repeat performance of hedge fund managers, or if that dispersion will narrow.

Major Risks to Expectations for 2023

-

Growth Collapses – The US GDP growth expectation (JP Morgan) for 2023 is 1%, which is a slowdown from 2022. If the US has a deep recession as a result of overtightening and asset prices collapse the equity markets will have a difficult time.

-

Inflation Crashes – In this case the Fed would not be forced to raise rates further and we can return to a <2% inflationary environment. If this were to occur, then Large Cap Growth stocks would be preferred as asset-light companies may reemerge to outperform.

Please contact your Wealth Advisor at Procyon Partners to discuss how this review may apply to your personal investment objectives. We appreciate your trust through these difficult periods of market stress. As always, we will continue to navigate the sometimes-treacherous waters of the global investment environment on your behalf.

Thank you for your continued support and confidence in the Procyon team.

Best Regards,

Procyon Partners

Download PDF BACK