Market Update – The Economy, COVID and Politics! – August 7th, 2020

With July 4th past, we have now celebrated the 244th US Independence Day! While we each celebrated in our own ways, even the most socially distanced conversations likely encompassed the same hot topics, including Covid-19, social unrest, and the upcoming elections.

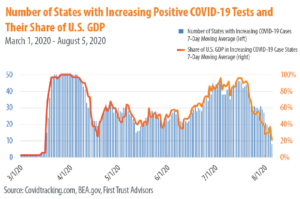

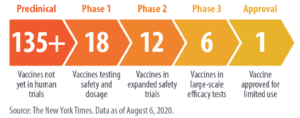

On the economic and investment fronts, the battle with COVID continues to drive much of the market activity. As we forecasted in our Procyon base case way back in March, this month we watched business activities fluctuate; progress waxed and waned. The continued spread of the virus has shown that communities with minimal initial impact are now just as vulnerable to the crisis. It appears new case counts are beginning to come down from the second recent peak. Billions of dollars are being poured into multiple vaccine trials and production facilities which provides hope that one or more will soon prove successful.

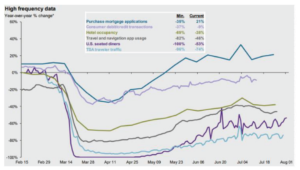

July provided further evidence that economic activity has improved since lockdowns were lifted, but high-frequency data indicates a recent pause in the US recovery. The overall data accelerated off its March lows, but the move higher has slowed over the course of the last month.

Global central banks took somewhat of a back seat during July, having already flooded the market with liquidity and taken rates to near zero. Though the European Central bank did announce financing of additional aid through bond issuance, governments have been under pressure to provide further fiscal support. As of this communication, the US Congress has yet to reach an agreement on the next stimulus package. The level and duration of unemployment benefits, aid to states, money for hospitals, money for testing as well as “non-COVID” riders are all being thrown around in Congress. Government is also contemplating additional aid to troubled sectors such as airlines. An eventual deal of some sort seems likely; although the political battles this time around have intensified to a new level as we expected, with our Base Case outlining a likely scenario whereby the political drag will increase as the perceived urgency of relief funding wanes and the elections move closer.

US GDP fell in the 2Q20 by an annualized rate of -32.9%, while it contracted by 5% in 1Q20. This was a record reflecting the sharp and swift drop off in activity driven by COVID-19 in the first few months of the pandemic.

US equities continued to advance. Large cap equities outperformed small and midcap equities for the month. The S&P 500 was up +5.64% while the Russell 2500 advanced +3.98% in July. Growth continued to outpace value during the month, +7.69% vs. +3.95%. Year to date growth equities have materially outpaced value by over 31%. International developed market equities trailed their emerging market counterparts in the month, +2.33% vs. +8.94% respectively. Both taxable and municipal fixed income moved higher in the month, with the US Agg Bond Index +1.49% higher and the Municipal Index +1.68% in July.

The Procyon Investment Committee continues to monitor several risks:

- Fiscal Help: The Federal Reserve has made it clear that they can only do so much. They are limited to lending and acknowledged that this crisis will require additional spending from the The Fed continues to purchase sizable quantities of Treasury and agency-mortgage- backed securities. Chairman Powell believes current legislation provides them the ability to buy qualifying corporate debt. However, at this time they have no intention and have not done the work to buy equities. We are hopeful the US Congress will pass an appropriate package in August. The risk would be no deal or a bad deal.

- Virus progress: The virus continues to spread globally and has not yet been contained. In continental Europe, Australasia and some parts of Asia, including China, new infections have fallen to low levels and economies are reopening. Spain is a current hot spot in Europe. In the UK, new infections have also continued to fall, albeit not to the low levels as experienced in Europe. India and much of Latin America have been unable to get the virus under control.

- US Elections: The sharply divided US electorate barrels towards the November Elections at full speed with the outcome Biden is leading in the polls in the four crucial swing states, but we saw how that played out in 2016 so there is an asterisk to the polling. So far, the market appears to be shrugging off Biden’s lead. With the house remaining in Democratic hands, the US Senate holds the key to determining whether we will have a divided, and thus more restrained, federal government in 2021. Our team is continuing to focus on potential policy changes in both directions and discussing various probabilities and the financial impacts.

The Procyon Investment Committee is proud of the work we are doing for our Private Wealth and Institutional clients during this challenging time. We continue to be focused, active and diligent as we chart the long-term path forward. In the coming months we will keep you well informed. As always, please call your Advisor if you have any questions around your personal financial situation. We are here to help, and we wish you and those important to you a safe and happy end to the summer.

Download PDF BACK