Welcome to Spring!

Spring cleaning takes on extra significance this year as we all look forward to ending what seemed like a long winter’s rest! We share the excitement of welcoming the warm fresh air after a year of lockdowns and beginning to close the history books on the Covid-19 pandemic.

- Market Update- Q1 2021

- Inflation Worries

- Stimulus

- Vaccine update and States reopening

- Tips for Spring Cleaning your Personal Finances

Market Commentary

The new bull market in equities continued through the 1st quarter in 2021 as both domestic and international markets ended the quarter in positive territory. The Russell 3000 (a broad measure of domestic US equities) finished Q1 up +6.35%, lifted higher by the strong performance of companies with small and mid-sized market capitalizations. Small and Mid-cap stocks were up +10.93%, outpacing large caps which were up +5.91% during the quarter.

International equities trailed their domestic counterparts, with developed international equities finishing the quarter up +3.48% and emerging market equities up +2.29%. Worth noting was the continued rotation into value-style equity names as well. This is a stark contrast to the growth-style outperformance leading us out of the pandemic lows. The MSCI ACWI Value was up +8.87% compared to the +0.28% return for the MSCI ACWI Growth. The dispersion between the two was even greater domestically, as value outperformed growth by 1070 basis points (as measured by the Russell 3000 Value versus the Russell 3000 Growth).

While equity markets were strong throughout the quarter, fixed income markets fell amidst the risk-on sentiment and rising interest rates. The Bloomberg Barclays Aggregate Bond Index finished the quarter down -3.37% while municipal bonds held up a little better, only down -0.35% (as measured by the Bloomberg Barclays Municipal Index). Safer fixed income sectors struggled as both treasuries and investment grade credit were impacted by interest rates moving higher. Treasuries finished the quarter down -4.32% and credit was broadly down -4.45%. Higher risk fixed income fared well amidst the risk-on environment, with high yield bonds finishing the quarter up +0.90%. International bonds struggled in the 1st quarter as well, but held up better than domestic fixed income, falling -1.90% (Bloomberg Barclays Global Aggregate Ex US Hedged).

The 1st quarter of this year also marked the one-year anniversary of the stock market lows on March 23rd of last year. We would be remiss to not mention the extraordinary performance we have seen since those market lows.

From March 23, 2020 to March 31, 2021:

- The S&P 500 (Domestic Large Cap Stocks) is up +80.26%

- The Russell 2500 (Domestic Small and Mid-cap Stocks) is up +120.38%

- The MSCI EAFE (International Developed Stocks) is up +65.88%

- The MSCI EM (Emerging Market Stocks) is up +77.53%

- The Bloomberg Barclays Aggregate (Taxable Fixed Income) is up +3.08%

- The Bloomberg Barclays Municipal (Municipal Bonds) is up +13.24%

Inflation, Bonds, Rates

Market performance, specifically in the fixed income markets, was dominated by inflation fears and the resulting rise in interest rates throughout the quarter. With another stimulus package approved during the quarter, and the possibility of further stimulus still on the radar, the amount of money being pumped into the financial system continues to grow.

At the same time, high frequency data is showing a rebound in consumer demand that picked up during the first quarter of this year. When you take these positive demand trends into account and review the current status and near-term outlook of global supply chains (which remain stressed

across several industries) it is understandable that inflation fears have crept into the market. While the catalysts are present for short-term inflation, long term expectations remain muted even with the Fed’s change in stance on inflation targeting. Despite moving higher since March of last year, 5-year forward inflation expectations are still just above 2%. It remains to be seen if CPI (Govt’ Inflation Measure) will pick up in the near term, but inflation expectations moving higher is enough alone to impact interest rates which is what we saw throughout the 1st quarter of 2021.

Interest rates rallied across the globe through the end of March, with the benchmark 10-year UST yield reaching a high of 1.77%. We saw short-term rates remain virtually unchanged as the FED continues to keep its target rate at zero and asset purchases remain in force.

The resulting economic story here is one that suggests an ever-steepening yield curve. This type of environment, where long-term rates go higher and short-term rates do not move up as quickly, is generally viewed positively and as a sign of confidence in future growth. Equity investments tend to perform well during this environment.

However, there are periods when holding too much capital in fixed rate investments can begin to erode purchasing power, and the potential for inflation can become a concern. The current environment is a growing concern for many global bond investors as evidenced by the accelerated selloff in February and March.

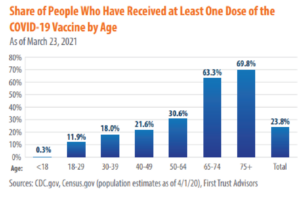

Vaccine / Reopening

The global vaccine effort is gaining momentum from its sputtered beginnings in 2020, with nearly 61 million Americans fully vaccinated and an average of 3 million shots being administered per day as of April 4th. The speed of vaccinations has also continued to pick up as the FDA issued emergency use authorization for another vaccine this quarter, this one from Johnson & Johnson and requiring only a single dose.

With these developments, President Biden has urged states to make all adults eligible for vaccination by May 1st, an encouraging sign for the US population and economy. In addition, the federal government is working to double the number of federally run mass vaccination sites, pharmacies and increase the number of community health centers directly receiving vaccines. These combined efforts will help the US reach herd immunity, which is broadly anticipated to be achievable once 70% of the population is vaccinated.

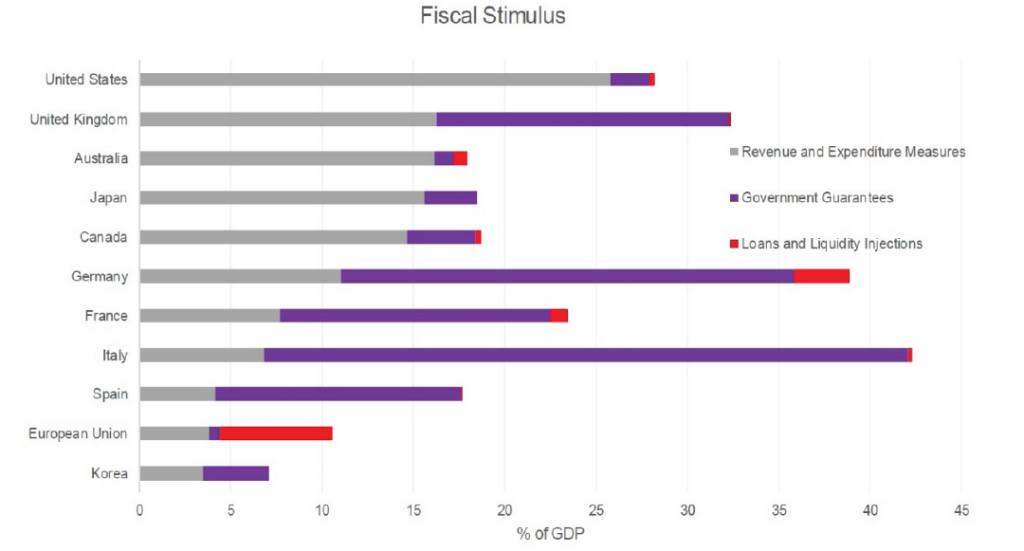

Stimulus

President Joe Biden signed a $1.9 trillion coronavirus relief package on March 11th to deliver another round of stimulus to the American people. The plan will send direct payments of up to $1,400 to nearly 160 million US households. In addition, while 20 million Americans are still claiming unemployment the bill will also extend the $300 per week unemployment insurance boost until Sept. 6th and expand the child tax credit for a year. It will also put nearly $20 billion into Covid-19 vaccinations, $25 billion into rental and utility assistance, and $350 billion into state, local and tribal relief. The legislation also addresses the Supplemental Nutrition Assistance Program by increasing the benefit by 15% through September and directs nearly $30 billion in aid to restaurants. Approximately $120 billion will be sent to K- 12 schools to assist in getting kids back to school.

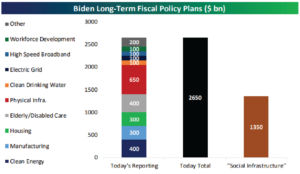

While there are still many questions surrounding long-term fiscal policy spending, we do have some early indications of where we might see the biggest impact. Physical infrastructure spending alone is expected to reach ~$650b. Jamie Dimon of JP Morgan Chase recently commented that given the stimulus and low interest rate environment, the resulting economic expansion could easily last through 2023. This is a major investment theme we will see play out in the coming years and we feel similarly to Mr. Dimon about the continued rapid expansion of the US economy. As our title suggests, “the grass is greener where you water it”, and as a result we will see a number of direct beneficiaries within the industrial, healthcare, energy and real estate sectors as mentioned in our recent Procyon Webinar

https://youtu.be/8v9zTM34lgE.

Spring Cleaning in Politics

While we suspended judgment for the first three months of President Biden’s administration, it is somewhat clear there will not be much compromise in Washington DC. President Biden has decided to “go big” in his words despite the narrowest of governing margins. The election cycle of 2022 has already begun. The only thing they may throw out is the Senate Filibuster!

The battles are not only in Washington DC but in numerous other states as well. Wisconsin, Pennsylvania, Arizona, and Georgia were the four closest states in the 2020 Presidential race. They are also the only four states expected to have tight races for governor and US Senate in next year’s midterms. The jockeying begins.

While there will always be politics, the level of distrust is very high, and a March CNN poll found 71% of Americans say political violence in response to election results is increasingly likely. The findings largely cut across party lines (78% D, 70% I, 65% R). Given that view one would hope we could collectively take steps to increase the confidence in US elections.

Personal Finance – Private Wealth

Since Procyon’s Private Wealth Advisors spend most of their time helping clients and families plan for their unique goals and objectives, we asked them to share some constructive Financial Planning tips to consider annually during this time of the year, as well as any updates that should be considered through 2021 so far.

- check your SS statement for last year’s earnings

- run an annual credit check

- complete 2020 taxes

- adjust 2021 withholding / pay 2021 ETP as necessary

2021 is proving to be an eventful year for clients’ personal financial planning. In March, a week after The American Rescue Plan (ARP) was passed, the IRS extended the Federal Individual Tax Filing Deadline as well as the deadline for retirement plan contributions to May 17th. However, estimated taxes would still be due April 15th, 2021.

While the American Rescue Plan’s provisions will impact our communities in different ways, it affects personal and professional finances generally in the following areas:

- Adjusted Gross Income (AGI) on your most recent tax return filed with IRS (e.g., 2019 or 2020)

- Tax filing status

- Dependents

- Employment status

- Type of employment

It is interesting to note that in the ARP the definition of “Dependents” has expanded to include children over age 17 and those who are financially dependent on the taxpayer. The windows of income eligible for benefits including the Recovery Rebates are very narrow. Phaseout ranges are as follows:

- Single Filers $75,000 – $80,000

- Head of Household Filers $112,500 – $120,000

- Married Filing Jointly Filers $150,000 – $160,000

Given many Americans experienced lower incomes in 2020 than 2019 due to the economy as well as the relaxing of Required Minimum Distributions (RMDs), it is possible that even if you were not eligible for relief payments in 2020, you might be eligible for benefits via the ARP.

Action: If you expect your 2020 AGI to be:

- Greater than 2019, consider waiting to file your tax return until you have the stimulus check in hand, as close as possible to the May 17 deadline

- Less than 2020, consider filing your tax return as soon as possible. Do not delay filing or request an extension to October; the IRS will only provide recovery rebate payments for 90 days after the Federal Tax Filing deadline

There were no references to Required Minimum Distributions (RMDs).

Action: Plan to collect your RMDs by December 31, 2021. We do not anticipate this requirement being relaxed again this year.

While there was no provision for student loan forgiveness, should forgiveness for a Federal and private student loan take place before December 31, 2025, the canceled debt will be tax-free. Previously, this canceled debt was considered taxable income.

Action: Stay tuned. What is important to note here is precedent. Now that student debt forgiveness is not considered taxable income, there is sufficient flexibility for future student debt reform to be negotiated and passed.

At the same time, there has been much speculation around tax reform in 2021. While there is a long list of proposed tax changes, the ones that have resonated the most with our clients include the following proposals:

Individual Income Tax changes

For filers earning $400,000 and up, e.g.:

- Increasing the income tax rate from 37% to 6%

- Capping the tax benefit of itemized deductions to 28% of value

- Phasing out the qualified business income deduction (Section 199A)

- Apply payroll taxes to build up Social Security

For filers earning $1,000,000 and up, e.g.:

- Taxing long-term capital gains and qualified dividends at the ordinary income tax rate of 6 percent

- Eliminating step-up in basis for capital gains taxation

Action: Use the documents you are already assembling this tax-filing season as a basis for analysis and appropriate action. Are there opportunities to make more tax-efficient decisions across your financial choices? Are you reducing your income today by maximizing your qualified employer retirement plan contributions?

Federal Estate Tax changes

- Reducing estate and gift tax exemptions, g.:

- Currently: this is $11.58 million per person and is scheduled to decrease to $5.6 million in 2026 according to current

- The proposed change is to reduce this to $3.5 million before 2026

- Increasing estate tax

- Currently the estate tax is 40%; this is proposed to change to 45%

Action: Revisit how much you are gifting to people and organizations important to you. Are the vehicles that you have chosen the most appropriate/tax-efficient? Now is a good time to (re)evaluate your gift and estate plans including:

- Donor Advised Funds

- Personal Loans

- Trusts

- Other vehicles to transfer assets temporarily or permanently?

As we reflect on what is required to enact tax reform legislation, we observe a lot of emotion on Capitol Hill with little precedent for bipartisanship (yet). The Senate’s use of reconciliation (majority vote), rather than traditional process, to pass ARP sets the stage for tax reforms to continue to be discussed this spring and potentially passed in the fall. Presuming legislation is passed, the next question is when it will be effective – retroactively? Upon signature? Beginning January 1, 2022? More to come, for sure. And as the information is confirmed, count on our team to guide you in interpreting it and applying it to your specific situation.

In closing we look forward to brighter days ahead…not only from the increased hours of daylight and warm sunshine, but also from the slow recession of the pandemic. There will be the inevitable “Summer thunderstorms” or “Hurricanes” to watch out for and navigate around – but those seem normal challenges compared to Covid. We look forward to returning to normalcy as soon as possible and wish you a glorious spring.

– The Procyon Team

Download PDF BACK