“Life isn’t about waiting for the storm to pass; it’s about learning to dance in the rain”

– Vivan Greene, 2006

So many questions swirl as we re-emerge from our homes and re-engage with our communities and activities. We have now been living in the COVID-19 pandemic for the last 4+ months and are all questioning the next phases for both our local communities and the country as a whole. Can we be comfortable now, or should we continue to isolate? Should we make the trip out to eat for the first time or should we wait another week? We are finding that the world around us adapts in its own way, as do we, yet we press forward, together.

In the coming months we expect several important issues to shift into the forefront as we all resume a semblance of normalcy as re-openings continue. The Procyon Investment Committee’s Base Case Scenario, first sketched out in our March 6th market commentary, highlighted a series of events that we track closely and discuss frequently as the data points evolve. Given that we are at the mid-point of 2020, we thought that we would revisit these scenarios and how they are playing out through the end of June. To recap:

Base Case: 60-65% probability

- Public health measures work to ‘flatten the curve’

- Steep decline in 2Q20 global GDP due to full shutdown

- Monetary and fiscal support continues

- Volatility spikes related to political and market stress

- COVID flareups as re-openings continue in waves across the US

Optimistic Case: 15-25% probability

- All base case points

- Speedy healthcare innovations related to vaccines or treatment of COVID-19

- Healthcare sector remains stable and proves able to handle influx of patients

Unfavorable Case: 15-20%

- High levels of lingering indebtedness and psychological effects of pandemic

- Crisis created by ineffective policy decisions leading to sustained decline in hours worked, wages, employment, and consumer confidence

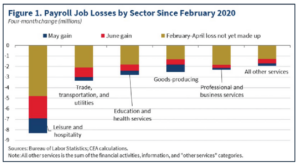

As a Committee we feel strongly that we are by and large experiencing the Base Case Scenario through the end of the second quarter, as outlined above and as evidenced by what we have seen in the preceding months. With states reopening and no vaccine delivery date we are watching infection rates, hospitalizations, and mortality rates in order to gain insight into how economies may react in the coming months. As we stand today, the US economy is weathering the storm by adapting quickly in our opinion. The job market added back approximately 7.5m jobs throughout May and June, and while the future of employment remains unclear, we believe our resilience relies on both adaptability and infection rates in the near future.

While we are seeing signs of consumer activity increase across almost all sectors, we are careful to note that 40% of companies have eliminated guidance for a large portion of 2020. There remains uncertainty around sensitive areas that are seeing capacity issues including global supply chains, healthcare, and education, forcing a growing number of companies to eliminate their expected sales and costs forecasts related to COVID-19.

As we continue to see lockdowns ease, it is likely that we may also see a false sense of safety set in for some citizens, resulting in an “all clear” approach to resuming daily activities. While we continue to learn about the virology of COVID-19, certain activities may result in additional outbreaks. As expected, we are witnessing some spikes in infections across the US through the second quarter and it is likely that we will see more as the pandemic grinds ahead. The resulting actions may lead to volatility in both employment and financial markets through the summer months, leading into the US Presidential election.

We have also seen massive support continue from both the Central Bank and the Treasury, with the US Treasury issuing ~$521b in Paycheck Protection Plan loans to over 4.9 million applicants. The SBA (Small Business Association) estimates that the businesses funded by the program support approximately 51m jobs. The Federal Reserve has communicated that they are committed to continued purchases across several asset classes including US treasuries, high yield bonds, mortgage securities and most recently, investment grade corporate bonds. They have currently purchased assets valued at ~$2.9T.

As a result of this economic support from the Federal Reserve and the US Treasury, domestic equity markets were able to post their strongest quarterly returns since 1987. US large cap stocks were up +21.82% (Russell 1000 TR) during the second quarter, while US Small & Mid (SMID) cap stocks posted a return of +26.56% (Russell 2500 TR) in the quarter. Despite the strong quarter, US equities remain negative for the year, with large caps down -2.81% and SMID caps down -11.05%. Investors also continued to favor growth stocks over value during the quarter with the Russell 1000 Growth outpacing the Russell 1000 Value +27.84% vs. +14.29%, respectively. This fiscal and monetary support was not limited to the US, as international governments and central banks took steps to support their economies as well. Developed international stocks were up +14.88% (MSCI EAFE NR) in the second quarter while emerging market equities posted a +18.08% (MSCI EM NR) return. The resurgence of risk assets extended into fixed income markets during the 2nd quarter as well. Credit markets were up +8.22% during the quarter as measured by the Bloomberg Barclays US Credit Index, while the Barclays US Treasury index (the safest fixed income) returned just +0.54%. Taxable bonds broadly outpaced municipal fixed income slightly throughout the quarter, +2.90% vs. +2.72% respectively.

As we look forward, volatility has ignited conversation around a number of reasons for another potential stock market selloff. As noted, we have learned that COVID-19 outbreaks may cause temporary selloffs in the coming months, however as we continue to inch closer to the November elections as well as the possibility of another round of stimulus, it is becoming increasingly clear that our attention is shifting to the future of national and economic policy. Politics aside, we are seeing building uncertainty surrounding the outcome of the election and the potential policy changes that may come with it. Evidence suggests that a divided government, by party, tends to limit extreme behavior and can provide stability in economic policy. There are increasing odds that we may not see a divided government come November, which would be a slight change in the details of our Base Case. While this is not yet sounding off an alarm, perhaps due to the country’s preoccupation with the pandemic, we expect there to be increasing dialogue about changes to our national policies related, but not limited, to: healthcare, unemployment, taxation, education and the national debt.

While questions around “what’s next” will continue, there is one thing you never have to question: our commitment to you. Our team is consistently by your virtual side. We are steadfast, focused, and vigilant, continuously monitoring this dynamic environment and committed to offering you perspectives in your best interest today, tomorrow, and always.

Procyon Partners

Source: Morningstar Direct, Data Analysis, 06/30/2020

Source: YCharts, Data Analysis, 06/30/2020

Download PDF BACK