A “Pre-Social Distancing” picture of your Procyon team!

Hello – You continue to be our top priority and as we close another dynamic week, we aim to keep you well informed during this stressful period. We understand you are juggling a lot right now.

- Service Update

- Making Lemonade

- Estate Planning

- Major Reactions

- Market Implications

Service Update: Procyon’s technology was designed from inception to be completely functional in a remote environment. Everyone has laptops and all our systems are accessible in the cloud. We hold ourselves to a very high service standard and strive to process every request as quickly as possible. However, we do interact with other firms such as custodians or investment managers who may ask for additional time to meet the volume of service requests coming during this tumultuous period. We ask for your patience if administrative tasks take slightly longer than usual. We also want to remind you to be extra vigilant as, unfortunately, this crisis will bring out increased cyber fraud activities such as fake outbreak maps, fake charities, malicious emails etc.

Making Lemonade: Here are some specific steps you could take to benefit from this period.

- Refinance – Look at refinancing your existing liabilities to see if it makes

- Oil – If you live in the northeast and depend on fuel oil to heat your home, consider locking in a delivery contract now with oil at prices not seen since the

- ROTH Conversion – If you expect your IRA to rebound, you could consider converting some or all of it to a tax-free Roth This depends on your personal situation and you would have to pay taxes on the converted amount (which is down) and would capture all the future upside in a tax-free account. We can work with your CPA to see if it makes sense for you.

- IRS Delay – While fast breaking news Friday, the IRS announced they will delay tax filing deadline to July 15th. The April 2020 estimated tax payment has also been deferred until then as well. This applies to both individuals and

- GRAT – For those clients with an estate tax concern, a GRAT or other asset transfer vehicle looks increasingly attractive due to the combination of low interest rates and temporarily compressed asset

Estate Planning: While this important topic is never anyone’s favorite, sadly this crisis has reinforced how important it is to have your basic estate planning documents in order. A will or living trust, durable power of attorney and a health care proxy are a must. If your documents are getting dusty in a drawer, why not make the most of the social distancing and dust them off to see if they still reflect your wishes?

Major Reactions: We received both fiscal and monetary policy relief this week as central banks and governments took increasingly forceful actions to assist the global economy and the medical crisis.

- The US Federal Reserve fired a bazooka on Sunday – Instead of waiting until the meeting scheduled for Wednesday, the Fed cut the funds rate by a full 1% and announced they would begin a version of Quantitative Easing 4 (QE4), though they didn’t call it that, when they said they would buy $700 billion of bonds to help lower interest rates and provide liquidity to some stressed markets. Third, they reduced the discount rate to 0.25% – this is the rate the Fed charges banks to borrow – to encourage institutions to tap the Fed as needed. Finally, the Fed did this in concert with global central banks. The Fed Chief Jerome Powell also said the Fed will be “patient” which means it’s going to be awhile before rates go back

- The European Central Bank (ECB) led by Christine Lagarde took similar actions as

- The US Federal Government passed a coronavirus relief bill, the Families First Coronavirus Response Act, that targeted paid leave and testing as a first step. Congress and the President are also at work on phases two and three focused on providing necessary relief to impacted citizens and industries. This could include direct payments to some Americans and, as currently discussed, cost $1 trillion or

- Isolation measures increase – Countries increasingly began closing or severely limiting their cross—border traffic as France, Germany, New Zealand, Australia, Canada and others try to slow the spread. We would not be surprised if the US was soon to follow as the city by city, and state by state rollout response appears slow and ineffective in getting ahead and “flattening the curve.” We know from talking to clients across the country that the seriousness and response efforts are viewed, at least initially, very

Market Implications: This past week was another volatile week for many markets. Globally stocks sold off and even bonds reacted to the size of the stimulus and market stress this week. Earlier this week as the equity markets approached -30% from their peak, bond prices began to fall as well. Over the course of history this is an uncommon phenomenon, however not completely unheard of. This can occur during a liquidity crunch, where leveraged investors begin to sell their safer securities in order to generate a cash position that could help shore up losses elsewhere. We saw similar activity during 2008-09 market sell off. However, this time the selloff appears much more orderly and controlled, especially given the enormous swings over the course of the last several weeks. Markets are functioning. We certainly don’t like what they are telling us about the immediate future, but they are working properly at this point. This is extremely important as we move from panic to ultimate recovery. The trust we put in our market infrastructure is monumental, and markets need to continue to function in order to produce price discovery that is accurate and liquid. We continue to monitor any developments related to market function in this stressful period.

Another implication present during the financial crisis and currently absent from the pandemic is panic surrounding our financial institutions. We are certainly seeing stress on equity and credit prices for our largest institutions, however by and large we feel the banks are in the best position they could have been to weather this storm. There are a few reasons we feel strongly on the subject, mainly surrounding the massive capitalization of major institutions. Over the last decade our systemically important financial institutions have been required to stockpile capital as a result of the leverage and subsequent insolvency of some large financial firms during the financial crisis. In addition, these firms have all been stress tested for massive losses on a regular basis by regulators. This is not to say we will not experience losses in the banking sector, we simply believe it does not represent the same level of risk as it had in previous market shocks. A functioning market and banking system are two key pieces of infrastructure and we see positives on both fronts.

Health Concerns vs. economic concerns

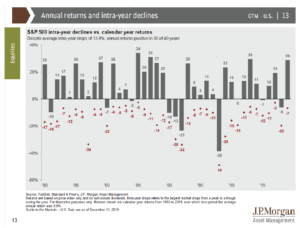

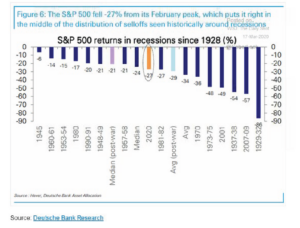

China, South Korea and (hopefully) Italy illustrate that the spread of the virus can be contained with drastic “social distancing” measures, but not without a hit to personal freedom and economic activity. The US case count will get worse before it gets better. The economy itself has likely tipped into a recession and may also get worse before it gets better. The process of finding a bottom in a bear market typically doesn’t happen overnight.

A Coronavirus Recession may sound like a reason to sell, but it’s not. Stocks typically rise starting 3 – 6 months before a recovery. We’re already in that window. It’s been proven time and again those who sell now are likely to regret it.

It is our hope that you will be aware and attentive, but do not be afraid. Moving to cash thereby locking in recent losses that we believe may recover is, in Procyon’s opinion, a mistake. Do not make long term changes over short-term dislocations.

Actively seek to avoid common behavior investment mistakes. In times of stress, many investors default to behaviors that can harm long- term performance. One example of this is home country bias, or reallocating to what seems to be a more known and comfortable market: your own. In this recent market downturn, however, many emerging markets have outperformed the U.S. markets on a relative basis, illustrating the potential benefits of a globally diversified portfolio. A second example is the gambler’s fallacy, in which investors believe they will “know” when to get into and out of the market. But this is almost universally false. Market timing is extremely difficult, and the empirical evidence suggests that individual investors are particularly bad at it. The better approach is to remain disciplined and stick with a long-term portfolio that was constructed to ride the waves of volatile markets.

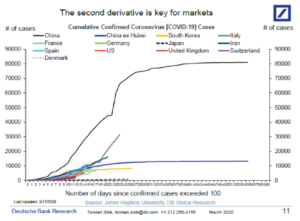

The market is forward looking and will react not when “things are good” but when they are “simply less bad.” In mathematics we call that the second derivative, measuring the rate of change.

These are uncertain times and we will strive to keep you informed, to help keep you calm and look for investment opportunities amid the turmoil.

In conclusion, rest assured that we are actively looking to manage your portfolio and find the best investments to help ensure your future success. As always, please reach out if you have any questions or concerns.

Download PDF BACK